February 20, 2019

Frances Donold, Head of Macroeconomic Strategy

The start of this year saw the return of risk-on sentiment as investors welcomed a newly dovish Fed and signs the Chinese economy is over the worst – but geopolitical tensions and the growth outlook are lingering concerns. Will strengthened stimulus from China and a solid economic growth in the US economy be enough to stabilise global markets? Frances Donald, Head of Macroeconomic Strategy within the Asset Allocation Team at Manulife Asset Management, examines the market fundamentals and economic issues underpinning the market’s rebound in early 2019.

Two significant macro events have supported a return to risk-on behavior, partly erasing the weakness seen in late 2018. First, China strengthened stimulus measures and markets began to adopt a view that the worst of China's most recent cyclical slowdown was probably left behind in 2018. Second, in early January, the tone of the Federal Reserve's (Fed's) communication appeared to take a dovish turn, suggesting fewer (if any) rate hikes ahead and more flexibility with respect to the Fed's balance-sheet tightening. Minutes of the FOMC's 19th December 2018 meeting released on 9th January1 – coupled with a very dovish statement and press conference2 following the FOMC's January 30th rate decision – reinforced that view.

These macro developments, combined with some oversold conditions in equities, generated four important global market reactions3:

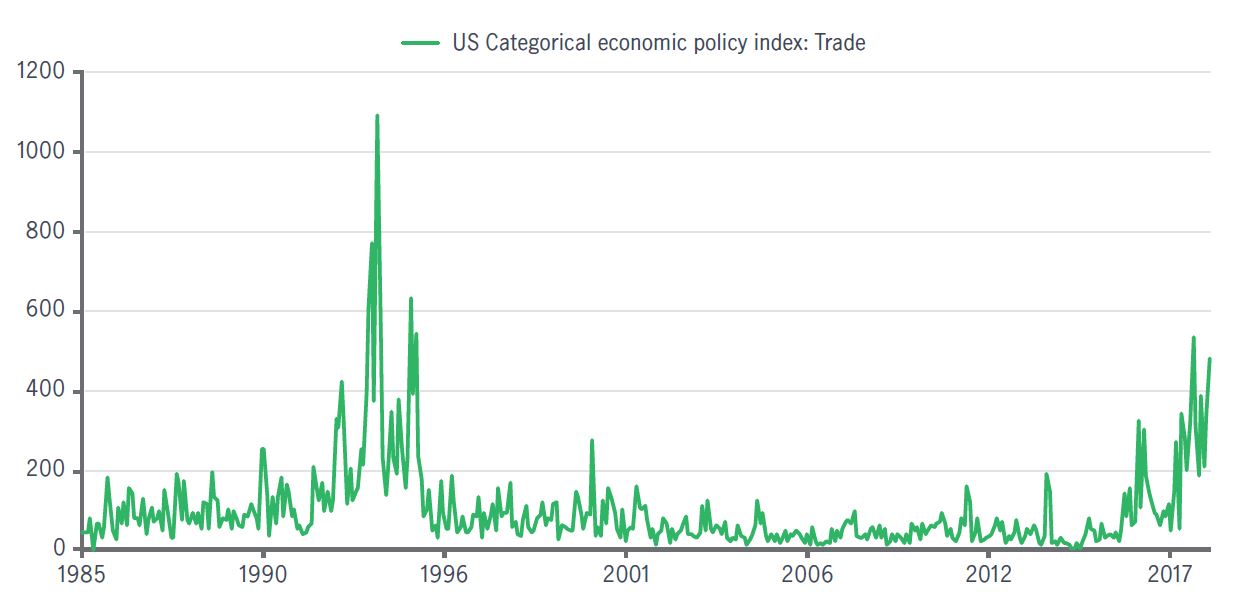

Meanwhile, geopolitical developments continue to produce headline risks that whipsaw global markets. These risks are challenging for market participants, in large part because they are difficult to quantify, model, or forecast, and yet they can significantly alter the economic outlook for several key countries. The US Economy Policy Uncertainty Index measuring trade uncertainty, for example, is at its highest level in almost 30 years4. This uncertainty continues, in our view, to encourage investors to seek safe havens more than might seem typical.

From the Asset Allocator's perspective, this continues to be a very tactical market in which we should expect persistent volatility. Even as Chinese and US policy makers have alleviated some near-term concerns, markets will be carefully assessing the global growth profile outlook, which continues to appear soft and worsening. We should expect heightened reactions to headlines, economic data, and central bank policy over the coming months.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Latest asset allocation views for Asia Q1 2026

Three key global themes for the first quarter: Liquidity and stimulus set the stage for 2026; AI remains a structural growth driver; Accelerating growth may favour diversification

Source: Bloomberg, Manulife Asset Management. As of 12 February 2019.

At the end of December, it became clear to us and to markets that China was moving from piecemeal, reactionary forms of monetary policy towards proactive, broad stimulus. This has provided a key support to EM, which relies heavily on Chinese growth and trade expectations.

The inflection point in Chinese policy has also supported global risk sentiment as expectations of a Chinese economic stabilisation feed through into an improved global growth outlook, at least at the margin.

What has China done so far?

The People's Bank of China (PBoC) has recently been deemphasizing the "neutral" component of its prior "prudent and neutral" monetary policy refrain and is now placing an emphasis on forward-looking flexibility. Indeed, three moves from the PBoC in the past two months indicate it is now in full-blown "easing" mode:

What’s next from policy?

We expect 2-3 additional RRR cuts in 2019, but perhaps more importantly, a complementary fiscal package that could include value added tax cuts and enterprise income tax cuts (to be finalised at the upcoming People's Congress in March) and additional local government bond issuance.

However, the timing and size of these additional forms of stimulus likely depends on: (i) US-China trade talk outcomes, (ii) Fed policy, (iii) the global growth outlook and (iv) Chinese corporate earnings. In our view, Beijing is not keen to undo its de-leveraging and de-risking efforts of 2017-18 and will likely err on the side of the least stimulus necessary to provide growth stabilisation, particularly with respect to property and credit markets. Premier Li's comments at the State Council's 14th January meeting that China will not utilise an approach that will "flood" stimulus into the economy8 reinforces that view.

Will this stimulus be enough to support Chinese growth and markets?

In our view, the stimulus injected so far can be sufficient to provide temporary 12-18 month stabilisation in the Chinese economy, mostly via improved investor confidence, Chinese market sentiment and the expectations of further easing ahead. There are, however, two important caveats. First, stabilisation isn’t likely to materialise in economic data for several more months as stimulus tends to have lagged effects on growth. Second, while stabilisation is on the cards, we are not expecting a meaningful rebound or upswing in growth. In order to witness a sizeable rebound, we believe major infrastructure or property stimulus would be needed, which seems unlikely to us.

In addition, we think it's worth highlighting that there were already some green shoots of stabilisation visible in the economy in the last quarter of 2018, including industrial activity, corporate credit and a recent acceleration in leading South Korean economic data points that should support a less aggressive decline in first-quarter growth statistics before a more solid stabilisation appears later this year.

All else equal, this growth stabilisation combined with additional rate cuts and corporate tax cuts should continue to be supportive of both Chinese bonds and equities.

Can Chinese stimulus and growth provide a tailwind to EM assets and/or global growth?

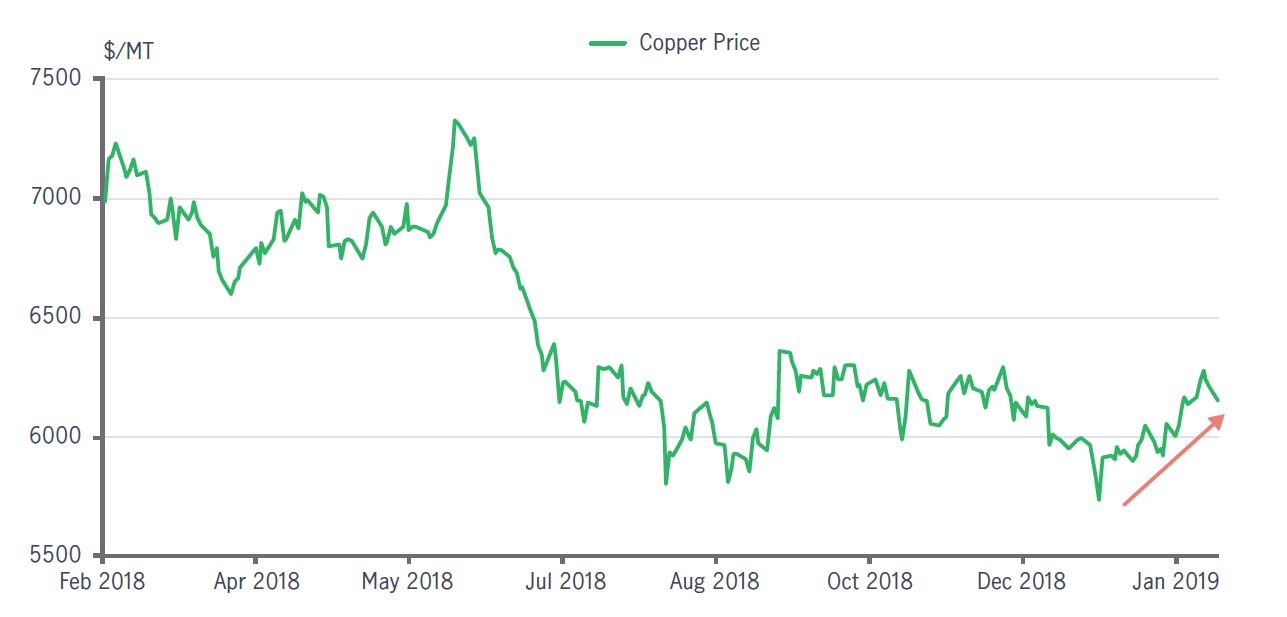

Once China's economic data does stabilise, we expect the global economy to feel the improvement with a three-to-four quarter lag. This means that the rest of the world's real economy is only likely to benefit late in 2019/early 2020, even if markets, such as China-tied copper prices, have priced in the improvement earlier in the year. For Europe, and Germany in particular, Chinese stabilisation is good news and mildly improves our outlook for European growth in the medium-term.

What does stimulus mean for your currency view?

Near-term resolutions or even improvements in US-China trade talks will provide short-term support to the renminbi and we expect policymakers are keen for the USD/CNY exchange rate to remain below 7.0 until there is more clarity on the trade and global growth outlook. However, narrowing bond yield spreads between China and the US and a shrinking current-account surplus are structural trends that are difficult to ignore. While we expect the USD/ CNY exchange rate to breach 7.0 in 2019, it seems more likely that this will occur in the later part of the year rather than in the near term.

Source: Bloomberg, Manulife Asset Management. As of 12 February 2019

We are generally sympathetic to the idea that a sizable growth slowdown could occur in 2020. The negative impact on growth created by tighter monetary and fiscal policy and the impact of tariffs already in the system are important. It's also clear that the US economy is in a late-cycle stage and that high non-financial corporate debt could produce additional headwinds to growth. However, the amount of "known unknowns" remains too large for us to feel comfortable calling a recession that far into the future. Plus, mitigating factors include how the Fed and other central banks respond to a weaker growth outlook, the evolution of Sino-US talks, and the potential for further global fiscal stimulus measures, particularly from Europe and China.

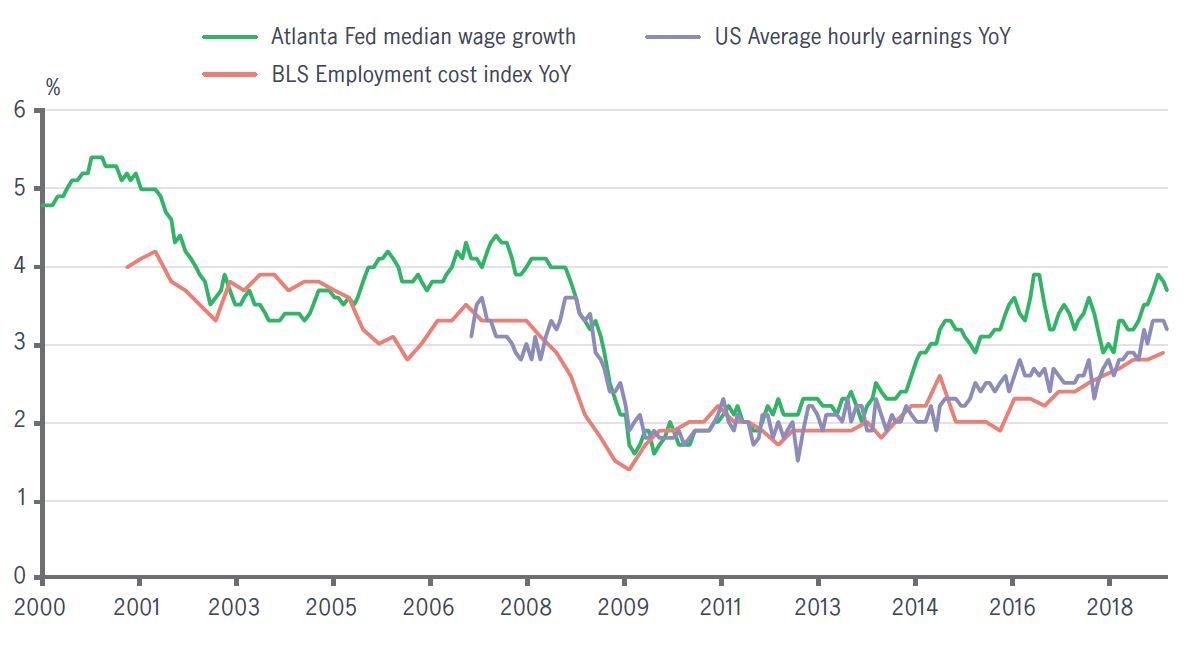

Right now, however, there are some important tailwinds in the US economy in the next six months that we believe are underappreciated. Most of these centre on the US consumer:

These potential upside surprises for growth are important because they will, in our view, pave the way for an additional rate hike from the Fed mid-year. Markets are clearly underpriced for this outcome, especially following very poor December retail sales data, with future markets pricing in less than a 10% probability of a rate hike by even the September 2019 meeting10.

If we are correct, bond yields will need to re-adjust and likely the front-end of the yield curve should make one last push higher in this cycle. That move will be larger if wage inflation is viewed as creating broader core inflationary pressures in the economy.

However, higher rates may also create some volatility around equities, particularly if the 10-year Treasury yield climbs back towards 3%.

Source: Bloomberg, Manulife Asset Management. As of 12 February 2019.

1 Minutes of the FOMC, 18-19 December 2018.

2 FOMC press conference, 30 January 2019; Federal Reserve press release, 30 January 2019.

3 Manulife Asset Management, Bloomberg, as of 12 February 2019.

4 Bloomberg, Manulife Asset Management. As of 12 February 2019.

5 People’s Bank of China press release: PBC launches TMLF to spur lending to small and private businesses, 21 December 2019. TMLF offers rates 15 basis points (bps) lower than the existing Medium-Term Lending Facility (MLF).

6 People’s Bank of China press release: PBC decides to lower required reserve ratio for financial institutions to replace certain medium-term lending facilities (MLF), 4 January 2019.

7 People’s Bank of China press release: PBC Launches Central Bank Bills Swap to Support Liquidity of Banks’ Perpetual Bonds, 24 January 2019. The tool was widely compared with “quantitative easing” because it’s an open-ended facility that could achieve considerable size. However, the tool is not currently buying fixed-income securities outright like other central bank QE programmes.

8 Reuters: China seeks good start to year to help hit economic targets, 14 January 2019.

9 Manulife Asset Management, Bloomberg, as of 12 February 2019.

10 Manulife Asset Management, Bloomberg, as of 12 February 2019.

© 2026 Manulife Investment Management. All rights reserved.