31 January 2023

Endre Pedersen, Deputy Chief Investment Officer, Fixed Income, Global

Murray Collis, Chief Investment Officer, Fixed Income(Asia ex-Japan)

Jimond Wong, Senior Portfolio Manager, Fixed Income

Eric Lo, Portfolio Manager, Fixed Income, Pan-Asian Bonds

Asian fixed income and its global peers faced a storm of unprecedented challenges in 2022- leading to a total reset for bond markets. Surging inflation amid higher energy prices, rising global interest rates, and escalating geopolitical risks, all contributed to a difficult global macro landscape. Meanwhile, idiosyncratic credit risks in the region spiked amid further ructions in China’s beleaguered property sector. Challenges inevitably persist as we move into 2023, but as Endre Pedersen, Murray Collis and the Pan-Asian Fixed Income team suggest, the risk-to-reward opportunities in the asset class for total return are improving amid a higher yield environment and an attractive spread premium. With potentially greater clarity in movement of rates and currency, credit should lead on stronger government policy, resilient economic buoyancy, and an evolving Asian credit landscape.

After a volatile 2020 and 2021, investors started the year cautiously optimistic about a more predictable market environment. However, these hopes were quickly dashed when Russia invaded Ukraine in February, which roiled global markets and amplified underlying inflationary pressures – particularly for commodities.

As oil prices surged and monthly inflation exceeded 8% in the US, levels not witnessed since the early 1980s, the US Federal Reserve (Fed) embarked on arguably one of its steepest monetary tightening campaigns in the post-World War Two period. The fed funds r¬ate jumped from a range of 0–0.25% (early March) to 4.25–4.50% (December), while Treasury rates surged from 1.51% (start of 2022) to exceed 4.20% (November).

Other major central banks (except Japan) and emerging-market central banks quickly followed suit by steadily hiking rates. China emerged as an outlier, as the country pursued a more countercyclical path to navigate the dual challenges of implementing zero-COVID restrictions and a deteriorating property sector.

This unique macroeconomic landscape presented exceptional challenges for fixed-income investors. The Bloomberg Global Aggregate Bond Index fell by 16.25% for 2022, while the JP Morgan Emerging Market Index moved lower by roughly 17.70%1. Despite the relatively short duration profile of Asian fixed income compared to global fixed income markets, China’s ongoing slump negatively impacted Asian fixed income markets most of 2022 until the government significantly eased zero-COVID policies and provided robust stimulus for real estate in November and December (For Asia’s yearly performance see Chart 1).

Asian investment grade credit demonstrated relative resilience, widening only 25 bps in 2022, mainly due to the region’s economic buoyancy and a large proportion of state-owned firms in the credit universe2. Total return contracted by roughly 10%3, largely driven by movements in US Treasuries’ yield. On the other hand, Asian high-yield significantly fell by roughly 15.10% for the year, largely driven by wider credit spreads and by uncertainty surrounding the future of China’s property sector4.

Chart 1: Market review of Asian local currency bonds, US dollar credits and currencies

Source: Bloomberg. JP Morgan Asia Credit Index. Index performance data shown in US Dollar, as of 30 December 2022. Past performance is not indicative of future results. Asian Investment Grade Corporate Bond Index = JACI Investment Grade Corporate Index; it tracks total return performance of the investment grade Asia dollar bond market, reported in US dollars. Asian Non-Investment Grade Corporate Bond Index = JACI Non-Investment Grade Corporate Index; it tracks total return performance of the non-investment grade Asia dollar bond market, reported in US dollars.

As we move into 2023, the global macro environment should, at the least, be more predictable and potentially more accommodating than this year. Indeed, while we certainly do not envisage a ‘rainbow’ after the storm of challenges experienced in 2022, we do believe the asset class faces fewer headwinds, or could potentially experience tailwinds in 2023. Overall, this presents more favorable risk-to-return opportunities and potential for a rebound after a year of ‘total reset’.

Our base case is that the Fed should move away from jumbo rate hikes (75 basis points), as illustrated in December’s meeting, and, as disinflationary pressures gradually build, then eventually pause. However, due to elevated inflationary pressures, we do not view a pivot to interest rate cuts as a high-probability event.

We believe Asia should be a primary beneficiary of this stabilizing macro environment as its growth profile remains resilient; however, the region could advance at different speeds. China’s faster-than-expected relaxation of zero-COVID policies and border opening should ultimately be a key driver for growth in 2023- although there are likely to be challenges along the way. Asia ex-China economies are also expected to benefit from this positive spill-over via increased trade and tourism depending on its economic ties with China. Overall, we believe this dynamic should contribute to investment grade’s continued performance and a potential rebound in high-yield with narrowing credit spreads.

In the next section, we break down our 2023 Asian fixed-income outlook into three areas: credit, rates, and currency.

After a difficult 2022, we believe Asian credit is poised to be the main contributor to fixed income returns in the new year.

China’s property sector has been a laggard in credit after the government assumed a new (unofficial) regulatory stance in August 2020 (‘The Three Lines’). The policies aimed to reduce leverage among some developers and the sector’s outsized contribution to GDP (previously 20–30% of GDP according to some estimates).

However, these policies contributed to a negative feedback loop: industry-wide deleveraging paused construction on existing projects and put new developments on hold. This raised uncertainty among consumers over the sector’s prospects who then sat on the sidelines, which further reduced cash flow for developers as sales of new properties stalled and housing prices fell further.

Zero-COVID policies arguably exacerbated the fall, as sporadic city-wide lockdowns prevented primary and secondary transactions and home buyers’ demand plummeted.

As a result, the sector had a challenging year: Numerous property developers were downgraded and defaulted; some initiated bond swaps; and upstream supply sectors faced bankruptcy. Without significant policy stimulus, many property credits traded at distressed levels for much of the year.

We believe that the government’s most recent policies released in late November have effectively put a floor under the market and bolstered investor confidence. While the sector's recovery should extend over the next two-to-three years; post consolidation it should ultimately emerge healthier with issuers that have sustainable debt levels and operate with greater economic efficiency.

Perhaps more importantly, we have also witnessed a significant change in the Asian credit universe over the past two years. While China real estate composed around 39% of the J.P. Morgan’s Asia Credit Non-Investment Grade index in December 2020, it has significantly contracted to roughly 13% due to defaults and index removals5. This has resulted in a less concentrated, more diverse credit universe in Asia that offers new opportunities to active managers.

Based on these new opportunities, our proprietary research leads us to be constructive on a few sectors in addition to China property in the new year: Macao casinos, China industrials, and India renewables.

Compared to 2022, there should be greater clarity over the trajectory of rates in the new year as the Fed’s monetary policy trajectory is relatively better communicated with less uncertainty.

This trend should benefit Asian markets that have experienced a wide dispersion in monetary policy across the region. Indeed, while the Philippines raised rates by 350 bps and India by 225 bps (both since May, others, such as Thailand, have only hiked by 75 bps (since August). A less restrictive global monetary environment should give more monetary room for Asian countries to promote economic growth and account for differing inflation levels without hiking to keep up with the Fed.

In 2023, we are particularly constructive on two markets: India and Indonesia.

India experienced a challenging 2022. While economic growth strongly rebounded from 2021 due to government stimulus and low base effects, rising inflation led the Reserve Bank of India (RBI) to pursue rate hikes aggressively. Accordingly, the 10-year government bond yield rose from 6.4% in January to 7.3% levels in November, its most significant year-to-date increase since 2017. In addition, JP Morgan deferred India’s inclusion in their Emerging Market Sovereign Bond index in November (placed on ‘positive’ watch), which led to foreign selling and reduced capital inflows.

Moving forward, we believe that the RBI has largely contained inflationary pressures, which should allow for a rate pause and a greater focus on driving economic growth in 2023. With further taxation reforms for foreign bond investors, inclusion of the country’s sovereign debt in global indices is possible in the new year, providing an extra boost for investors.

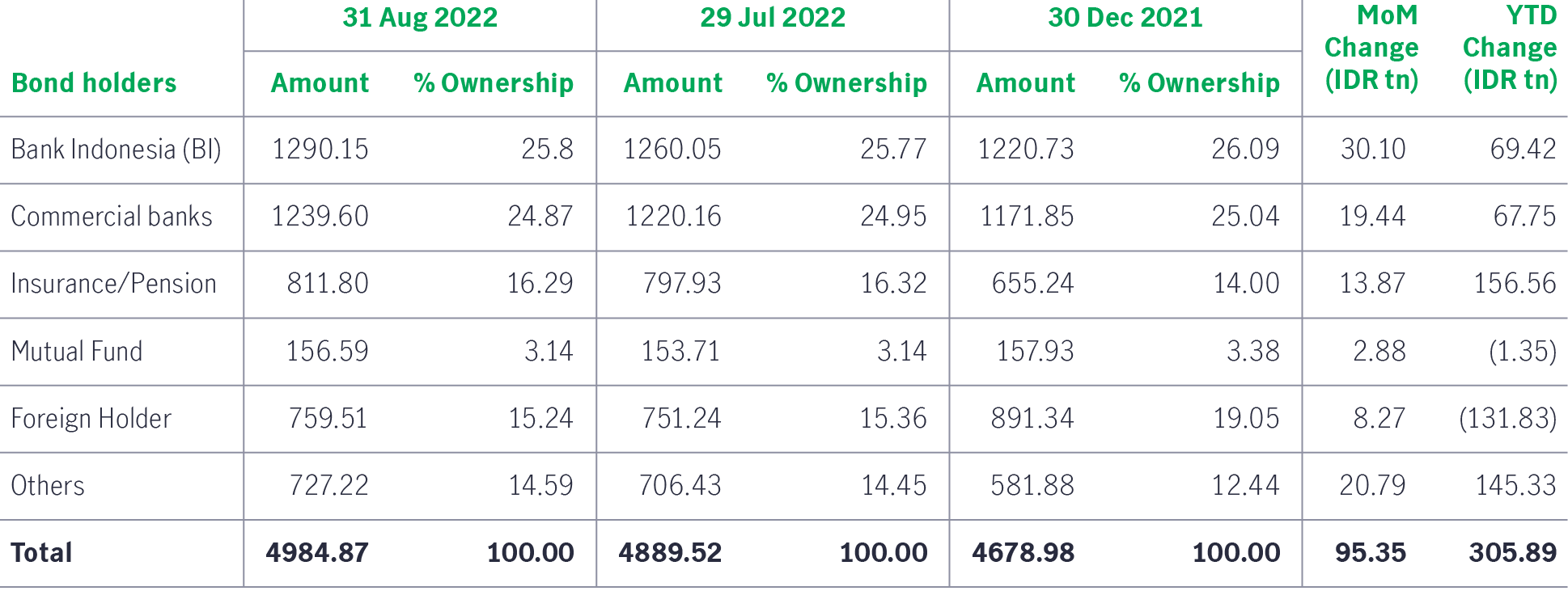

Indonesia experienced a volatile but resilient 2022. Bank Indonesia continued its ‘burden-sharing’ program with the Ministry of Finance to purchase government debt, which helped to contain rates throughout the year. As detailed in previous outlooks, foreign ownership of local-currency bonds has steadily declined over the past two years- from nearly 40% at the end of 2019 to roughly 15% at the end of August 20227.

This has led to a more diverse group of domestic stakeholders holding government debt for the long-term, particularly local commercial banks and pension funds (see Chart 2). More importantly, this ownership change has dampened the previous negative dynamic of foreign bondholders selling during bouts of heightened global volatility, driving local yields higher and weakening the Rupiah.

Chart 2: Foreign ownership of Indonesia’s local currency bonds have declined

At the same time, the country benefitted from robust global demand for commodities, as the current account remained in surplus (1.3% of GDP in the third quarter) for the year. Consequently, the Rupiah has posted better historical performance during prolonged volatility.

In 2023, we believe the country should have greater policy flexibility. With the central bank’s current strategy of front-loading hikes and providing targeted energy subsidies in the new year, inflation pressures are expected to fall. At the same time, the currency should face a more favorable macro backdrop and continued stability through the country’s current account surplus and easing US dollar strength.

The US dollar outperformed in 2022 on the back of higher rates and surging Treasury yields. The US Dollar Index (DXY), a measure of the greenback’s strength against major currencies, moved higher by roughly 8.2% in 2022, while the J.P. Morgan Asia Dollar Index, a proxy for Asian currency strength, fell by 6.4%8.

Moving into 2023, we believe that broad US dollar strength is likely behind us as Fed rate hikes are fully priced into markets. Furthermore, the impact from China’s faster-than-expected reopening could have a positive spillover to other Asian economies and currencies. We are constructive on the following high-beta currencies to the greenback in the new year:

After the storm of unprecedented challenges in 2022, we believe Asian fixed income is positioned to move from bearer of headwinds to beneficiary of tailwinds. The rebound in the asset class after November backed by Chinese policy stimulus and quickened reopening should be a key catalyst to watch in the new year.

Overall, we see attractive risk-to-reward opportunities among certain segments in the asset class. Higher Asian corporate bond yields could provide investors with relatively attractive entry points for total return and income investors. We believe that bottom-up credit selection will be the key driver in generating further returns going forward. Asian currencies are also poised for better performance with a weakening US dollar and resilient regional growth prospects.

1 Bloomberg, as of 30 December 2022, Indices used: LEGATRUU and JPEIDIVR.

2 JACIICBS Index, as of 30 December 2022.

3 JACIIGTR, as of 30 December 2022.

4 JACINGTR, as of 30 December 2022.

5 Source: J.P. Morgan as of 30 December 2022.

6 Known as three arrows because they aim to improve sentiment via bank credit, bond issuance, and equity issuance.

7 Source: IMF, Bank Indonesia.

8 Source: Bloomberg as of 30 December 2022. DXY and ADXY

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

© 2026 Manulife Investment Management. All rights reserved.