29 December 2021

Jimond Wong, Senior Portfolio Manager, Fixed Income

Neal Capecci, Senior Portfolio Manager, Fixed Income

Asian fixed income markets experienced a challenging 2021. Regional economies gradually recovered from the COVID-19 pandemic, while regulatory changes and idiosyncratic risk in some markets contributed to a divergence in performance between investment-grade and high-yield credits. In this 2022 Outlook, Jimond Wong, Senior Portfolio Manager, Fixed Income, and Neal Capecci, Senior Portfolio Manager, Fixed Income, outline why they believe Asian fixed income is poised for a rebound next year and highlight the significant opportunities available in the asset class for active managers. As always, robust credit research and strict credit selection are essential to find the right names in a fast-changing market.

Asian fixed income experienced an eventful year in 2021. Two macro factors played an important role for the asset class's performance:

Against this macro backdrop, Asian credits' performance sharply diverged in 2021. The J.P. Morgan Asian Credit Index (JACI) declined by roughly 2.3%. This figure, however, masked the notable divergence between investment-grade (IG) and high-yield (HY) credits: The JACI IG index has been broadly flat (year-to-date), but the JACI HY index declined by roughly 11% over the same period1.

Several reasons explain the divergence. Since July 2021, the Chinese government announced a raft of measures that changed the regulatory landscape in economically and socially important industries such as the internet and educational services (after-school tutoring).

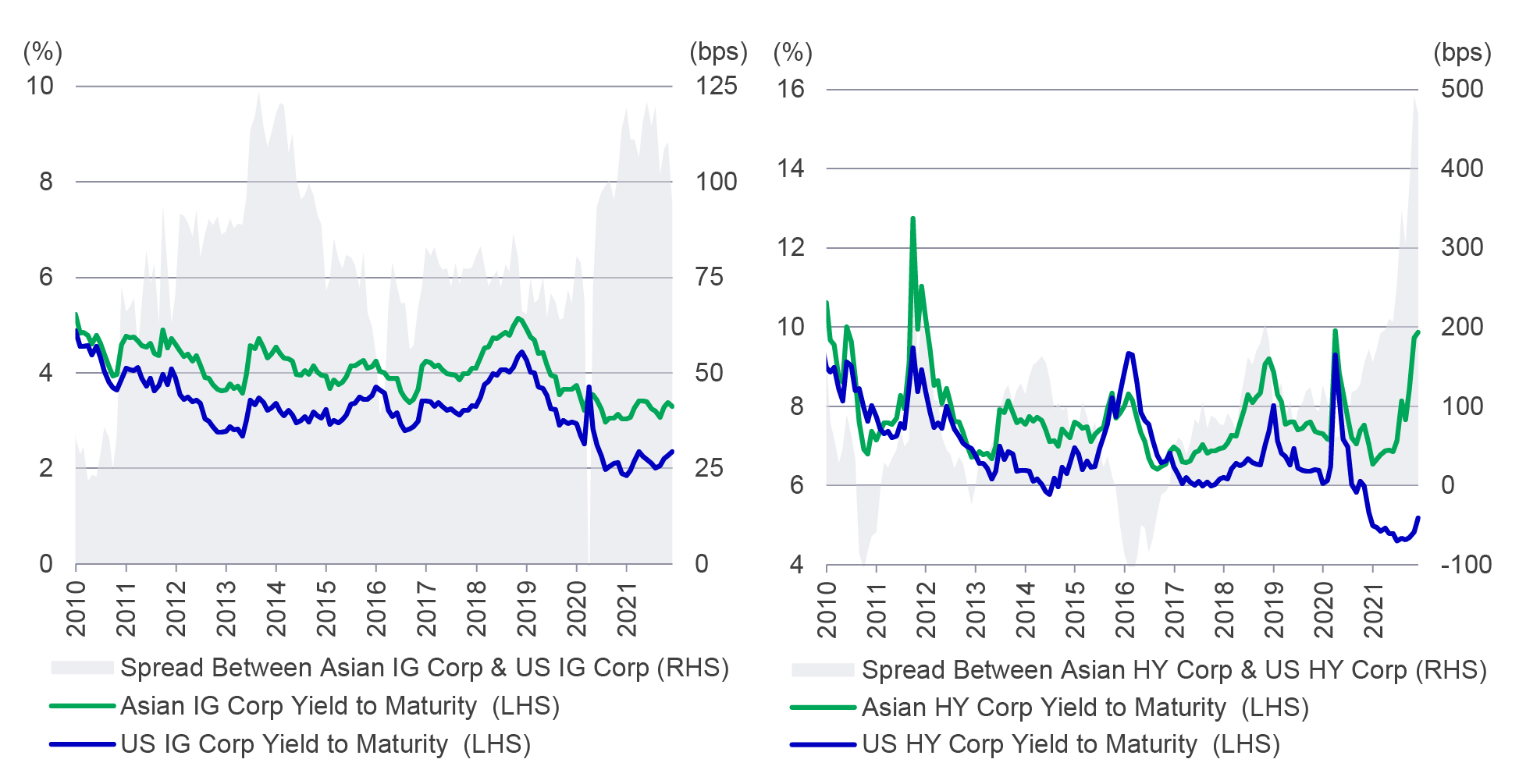

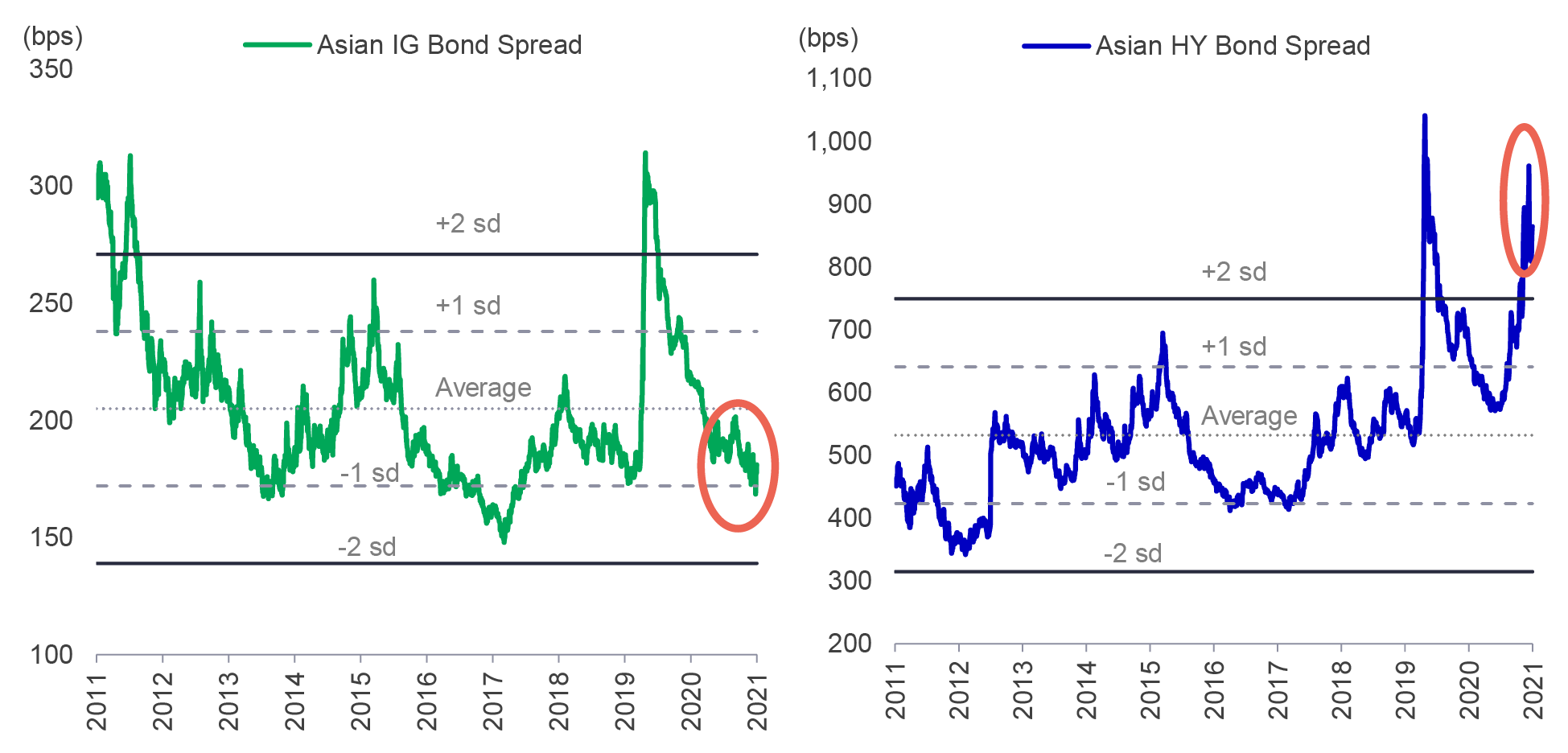

Even more crucially, previous regulations released in the real estate sector, such as "The Three Red Lines" policy, introduced in August 2020, had limited debt-related funding for overleveraged firms such as Evergrande, the second-largest developer in China at the time. In September 2021, the firm failed to make a series of payments on its onshore bonds and investment products2, which quickly spread to the rest of the sector and roiled investor confidence, catalyzing a sell-off in offshore Chinese property bonds and resulted in a significant drag to the US-dollar high-yield market3. Evergrande and a few other developers ultimately entered restricted default during the fourth quarter4. The price dislocations caused by these events have created notable opportunities for investors in Asian fixed income. Indeed, as Chart 1 shows, the credit spread premium for Asian credits (over US credits) in both IG and HY are roughly at decade-highs. We believe that high-yield valuations are particularly attractive as shown in Chart 2, with bond yield spreads well above historical averages, providing significant opportunities next year.

Chart 1: Asian credit spread premium at near-term highs

Source: Bloomberg, BofA Merrill Lynch and JP Morgan indices, as of 30 November 2021. Indices used: JPMorgan Asian investment grade corporate index (JACIICTR Index), JPMorgan Asian non-investment grade corporate index (JACINCTR Index), BofA Merrill Lynch US investment grade corporate index (C0A0 Index) and BofA Merrill Lynch US High Yield index (H0A0 Index).

Chart 2: Asian HY spreads particularly attractive

Source: Bloomberg, as of 30 November 2021. Asian HY bonds are measured by JPMorgan Asia Non-Investment Grade Corporate Index; Asian IG bonds are measured by JPMorgan Asia Investment Grade Corporate Index. Investment involves risk. Past Performance is not indicative of future performance.

Moving into 2022, we believe that credit will most likely present the most compelling opportunities for Asian fixed income investors. However, we are also constructive on selective opportunities in rates and currencies.

Overall, we see global liquidity to remain relatively accommodative from a historical perspective for Asian credits in 2022. We believe that attractive opportunities will exist in the Asian credit space throughout 2022, especially the HY segment, which we think some credits are excessively priced to the downside. Indeed, price dislocations, particularly in the China real-estate sector, that were experienced in 2021 do not reflect the underlying fundamentals of higher quality developers.

That said, robust credit research and strict credit selection are needed to find the right names that have value in this fast-changing market – characterised by consolidation, uneven recovery, and challenges in the weaker areas of the market. We are constructive on various high-yield segments across the region that offer not only competitive yields but also offer attractive valuations and diversification properties:

China: Property

The sector was heavily sold-off in 2021 due to negative news flow, concerns about rising defaults for HY issuers, and uncertainty over its future economic role and broader contagion risks. The volatility, however, also offers investors like us – who previously underweight the sector – opportunities, as we believe the market has priced in excessive default rates. We see it an opportune time and environment for active investors to navigate the cycle, as market weakness is likely to bring out value opportunities in fundamentally strong issuers that can steer through this episode unscathed, which will help generate further potential returns. Many quality companies are now being offered at compelling valuations with attractive entry points.

In 2022, we are likely to see greater consolidation in the sector amid continued challenges, as stronger firms (state-owned and larger private firms) recover and may take the opportunity to acquire projects from weaker or smaller-scale firms (or projects from them). More robust firms are also likely to benefit as they hold valuable collateral (projects) and benefit from government policies.

Indeed, we are beginning to see policy easing, such as relaxed mortgage approvals, eased onshore bond issuance for Chinese property developers. The People’s Bank of China cut the reserve requirement ratio (RRR) for banks by 50 basis points (bps)5 to stabilise funding channels prudently.

As a result, we are now overweight the sector. However, we are highly selective when choosing the winners that can navigate this cycle given the highly fluid situation. Overall, the sector is unlikely to return to its previous significant scale after years of over-investment; it’s also unlikely to maintain strong yearly sales growth with the wide margins seen in previous cycles. Yet, we believe that reforms (e.g., common prosperity) have made it more sustainable over the long term, particularly as real-estate developers have deleveraged and systematic risks are gradually reduced.

India: Renewable energy

Apart from China and the property sector, we are constructive on other strategic opportunities emerging in the region that remained resilient, particularly in India. Although some Indian credits may offer a relatively lower yield, they are generally more stable and less correlated to volatility in the broader asset class – which serve as asset allocation tools to manage risks and maximise value. Additionally, Moddy's upgrade of the country's outlook from "negative" to "stable" in October has reduced the fallen angel risk of its sovereign rating.

We are optimistic about the renewable energy sector, which we believe should rise in importance as the government recently declared its pledge to become net-zero by 20706. Companies offering renewable energy solutions should benefit from increased government support and an expanding market for their products and services. These credits also help bolster the resilience and enhance the ESG characteristics of the portfolio.

Asia: Bank capital

Finally, we are also positive on Asian bank capital bonds. Issuance in this area is still relatively new to the region, compared to more developed markets, such as Europe and the US, as banks previously sought other channels for funding. As capital needs have increased, high-quality, SOE state-owned and quasi-SOE banks in China, India, and Thailand have issued debt that we believe offers a compelling proposition for investors. Most issuers are large banks with some type of implicit government support. Indeed, due to the importance of banks to the overall economic landscape in Asia, governments and regulators maybe more likely to step in. Seasoned investors will typically move down the bank’s capital structure to find a particular segment that offers an attractive risk-to-reward profile, and many of the valuations available are more compelling than similar offerings in developed markets.

In 2022, we expect issuance in this space to increase, and investors will be looking across the region to add to their portfolios selectively.

In Asia, regional central banks should begin or continue to normalise monetary policy, although the pace and degree may vary greatly due to the pace of economic recovery and inflation, with the recently discovered Omicron COVID variant being a wild card.

Indeed, we currently see Asian central banks along the monetary-policy spectrum: Bank of Korea has already raised rates by 50 bps to 1.00%, the Reserve Bank of India stopped bond purchases in September and may increase rates in 2022, whilst Bank Indonesia has pledged to continue its "burden sharing" agreement into next year.

We are generally more constructive on short-duration bonds to mitigate interest-rate risk based on our current rate views. Regionally, we are negative on Singapore and Thai government bonds and the long end of the Korean government bond curve, which is more highly correlated with US Treasuries.

We are also constructive on two markets for longer duration in 2022 and beyond:

China:

After emerging early from the COVID-19 pandemic, the country’s growth momentum has declined on a sequential basis in 2021. This trend may continue into 2022 due to continued regulatory reforms, disruption in the real-estate sector, and residual COVID-19 risks.

Concurrently, government bond yields have remained at attractive nominal levels in 2021 (2.86% as of 30 November 2021), as the government implemented tighter fiscal policy, with China’s fiscal impulse estimated at roughly -2.5% of GDP. Monetary policy also remained selective and prudent, as the People’s Bank of China largely refrained from significant liquidity injections and did not engage in QE.

In 2022, we expect further monetary loosening after the recent RRR cut of 50 bps in early December. Indeed, the transition of the property sector and other regulatory changes should also result in some moderate loosening of China’s fiscal stance, while additional credit and regulatory easing could provide relief.

This should be constructive for China’s government debt and provide attractive counter-cyclical diversification for bond investors in a world of rising rates in developed markets. See our 2022 China bond outlook for more insights.

Indonesia:

The country was arguably one of the hardest hit regionally by the pandemic, entering recession for the first time in 22 years. The government responded with strong fiscal stimulus and import bans, as well as forging a “burden-sharing” arrangement with Bank Indonesia. The agreement mandated the central bank to fund the fiscal deficit through direct purchase of government debt in auctions. This arrangement was recently extended through 2022.

Indonesia’s robust policy response has created unique opportunities for bond investors by changing it from a foreign driven to a more domestically driven rates market. Previously, the country suffered from a chronic current account deficit primarily funded by significant foreign investor purchases of government debt. If there was a sell-off in the local bond market or global-risk off sentiment, the rupiah would also depreciate, creating a negative feedback cycle.

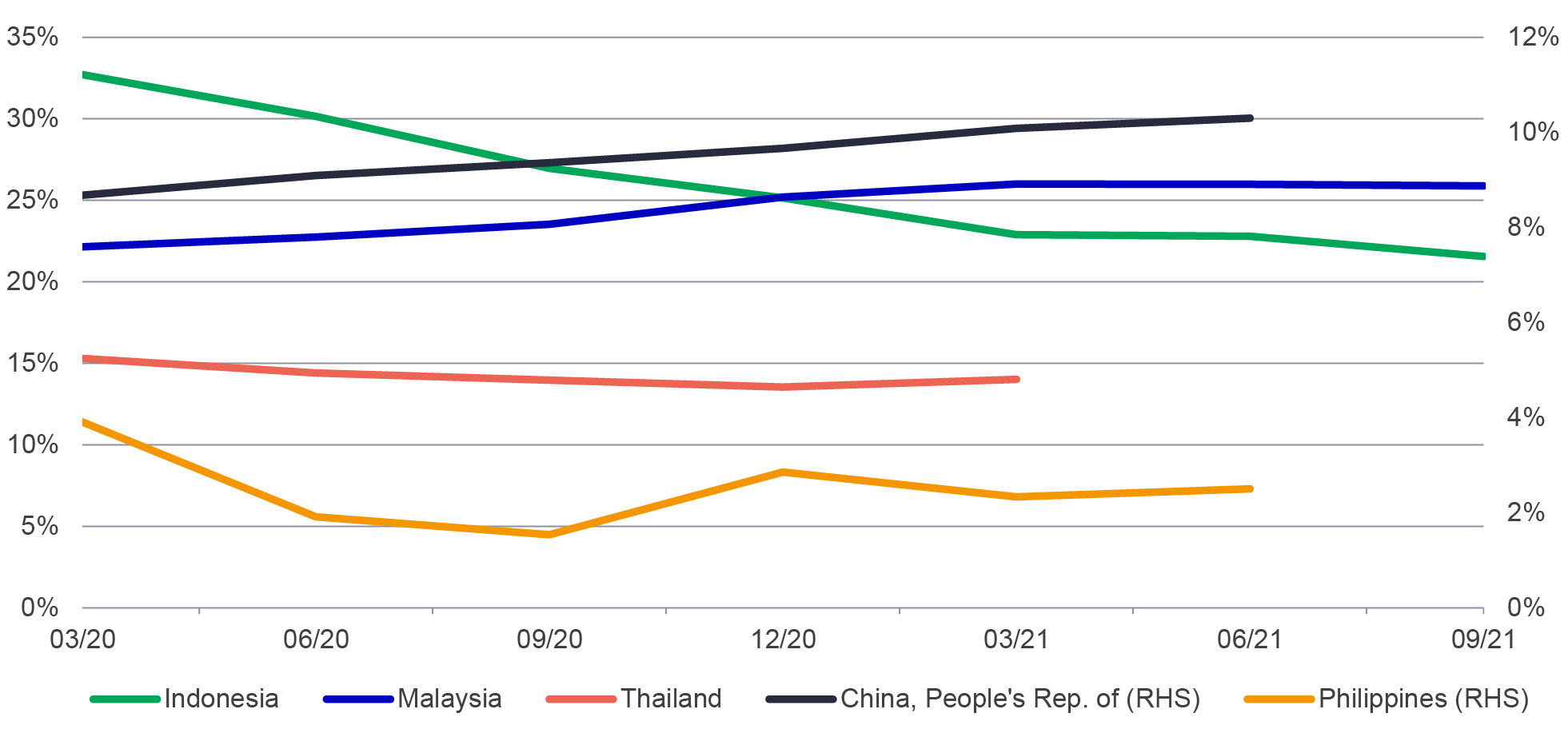

The newly adopted policies, coupled with a surge in commodity prices, resulted in the country posting its largest quarterly current account surplus in 12 years in the third quarter (1.5% of GDP). In addition, Bank Indonesia’s purchase of government debt has significantly reduced foreign ownership, from approximately 27% in September 2020 to roughly 21% in September 2021 (see Chart 3), with the central bank owning more rupiah debt for the first time ever; this has notably decreased volatility for local-currency bonds and stabilised the rupiah.

On the back of these developments, we are tactically constructive on Indonesia in 2022, and believe the market holds promise over the mid-to-long term.

Chart 3: Foreign holdings of Asian debt

Source: Asia Development Bank, as of September 2021.

Finally, we are more neutral on India. On the one hand, potential inclusion in global government bond indices could happen as early as the first quarter of 2022, which would be a positive demand factor for the market. On the other, stronger-than-expected growth in the second half of 2021 may lead the Reserve Bank of India to normalise interest rates faster than expected, posing a headwind for the short-end of the curve.

Thus, we are negative at the front-end of the government bond yield curve while positive on 5 and 10-year tenors, which provides a relatively higher nominal yield and carry potential.

Most Asian currencies, except for China’s renminbi and Taiwan’s new dollar, weakened against a resurgent US dollar in 20217. While the regional currency landscape is likely to be fluid in 2022, we are constructive on two currencies:

Thai baht:

Thailand’s economy was severely impacted by the COVID-19 pandemic, with pre-pandemic tourism composing roughly 20% of GDP and total employment. More importantly, the income earned from foreign tourists contributed to Thailand’s strong external position – a perennial current account surplus. With border closings and mobility restrictions, the current account surplus swung to a deficit in 2021 (3.6% of GDP September), leading the baht to become the worst-performing regional currency in 20218.

Although significant uncertainty persists with the recent discovery of the Omicron variant, we believe the baht is poised to recover some of that lost ground in 2022. Indeed, Thailand reopened to foreign tourists in November 2021, and with the vaccination rate trending higher, roughly 62% of the population is fully vaccinated, mobility restrictions are being lifted and fundamentals improving.

Korean won:

Korea’s economy has fared better than most in the region, particularly on the back of record exports. However, we are mindful the country’s representation in the emerging market (EM) equity index means that the currency tends to weaken during periods of underperformance, and investor selling, which occurred in 2021.

With continued projected strength in the Korean economy, we envisage the won is poised for better performance in the new year.

Although Asian fixed income experienced a trying 2021, we believe the asset class is positioned for better performance in 2022.

Indeed, the price dislocations experienced the year afford investors a rare opportunity to take advantage of near-term highs in the IG and HY credit spread premium over US credit as well as idiosyncratic credit opportunities. With increased volatility, and likely further unknowns, however, robust credit research and strict credit selection will remain imperative for investors to take advantage of all Asian fixed income has to offer.

1 Bloomberg; data as of 15 December 2021. General Asian credit is represented by JACICOTR (Bloomberg code); investment grade is represented by JACIIGTR; and high-yield is represented by JACINGTR.

2 Reuters, 30 September 2021.

3 Bloomberg, as of 21 September 2021.

4 Bloomberg, as of 16 December 2021.

5 Bloomberg, 6 December 2021.

6 Bloomberg, 1 November 2021.

7 Source: Bloomberg. Year-to-date returns as of 15 December 2021.

8 Source: Bloomberg, as of 15 December.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Latest asset allocation views for Asia Q1 2026

Three key global themes for the first quarter: Liquidity and stimulus set the stage for 2026; AI remains a structural growth driver; Accelerating growth may favour diversification

![]()

©1999 - 2026 Manulife Investment Management (Hong Kong) Limited