31 December, 2020

Despite a challenging 2020 for investors, Asian equities provided one of the few bright spots globally. After the COVID-19 outbreak, segments of the region contained the virus more effectively than others, leading to a divergence in economic and equities’ performance in the second half of the year. We believe that while Asia (ex-Japan) is tapped to strongly rebound in 2021, divergences should remain, giving investors attractive opportunities in a region that is greater than the sum of its parts.

The past year posed unprecedented challenges and opportunities for investors. The global outbreak of COVID-19 in the first quarter of 2020 roiled markets and economies alike. Although North Asian economies were the first affected, they were also among the first to effectively contain the spread of the virus, with some avoiding entering a technical recession1.

In contrast, South and South-east Asian economies were affected later, but due to higher population density and less developed health systems, bore a heavier cost of the pandemic. India and some ASEAN economies (most notably Indonesia) fell into technical recession for the first time in decades.

Robust fiscal and monetary stimulus globally and in Asia allowed equities to recover, with regional equity indices posting a nearly 19% return2, but with significant dispersion in performance across the region3.

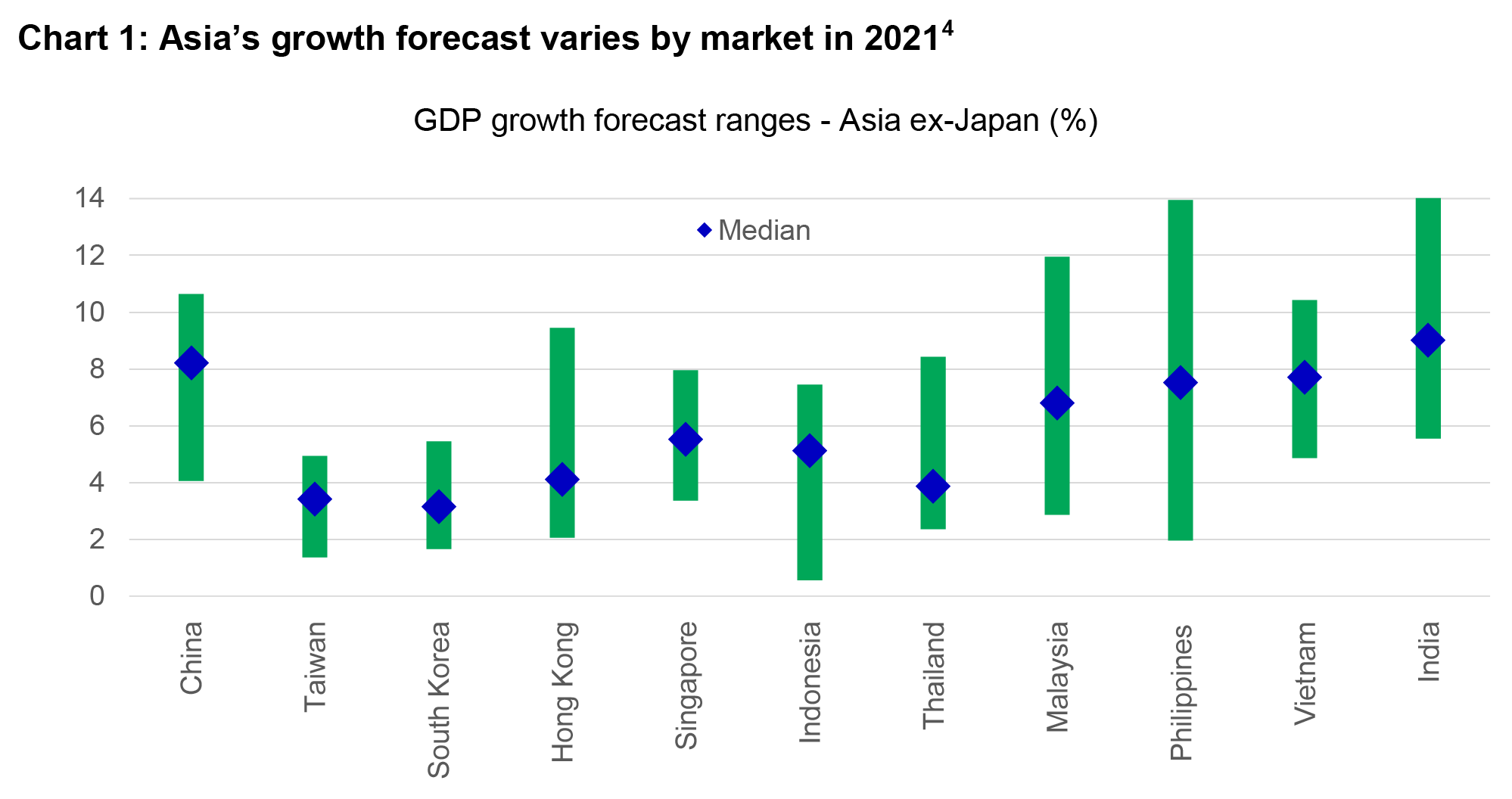

Moving into 2021, the region is tapped to strongly rebound at roughly 5.5% growth overall4; however, this comes from a lower base and we anticipate economic recovery to be gradual and uneven due to varied policy responses as well as divergent access and rollout of vaccines in Asia (see Chart 1).

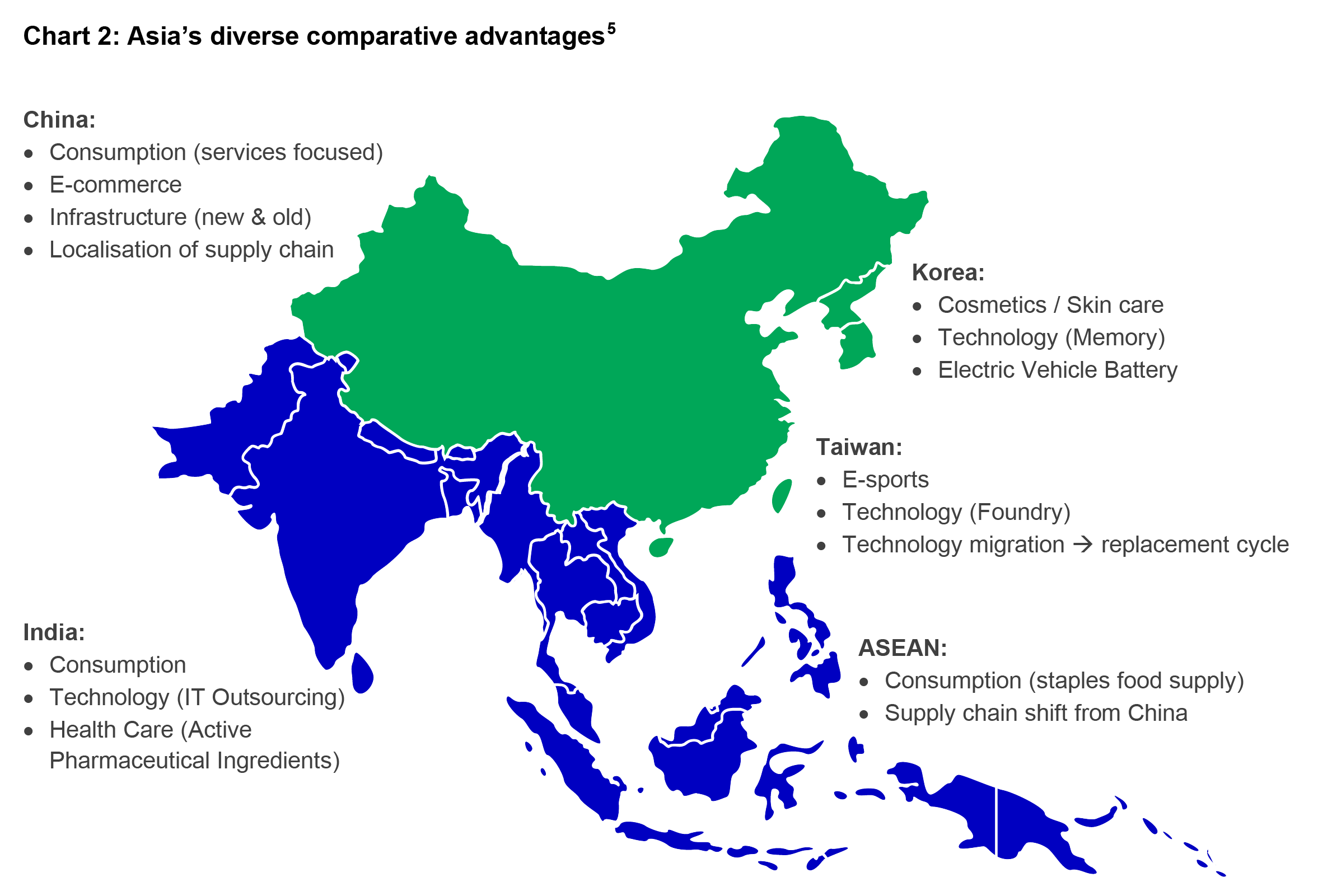

Before exploring the major regional themes for 2021, it is important to understand how we view long-term investment opportunities in Asia. Indeed, investors should be vigilant that with optimistic economic growth forecasts and elevated valuation in some regional equity markets, it is necessary to understand where sustainable, long-term growth can be achieved rather than a cyclical upswing as economies recover from the shock of COVID-19.

As Chart 2 shows, we envision the region as possessing a diverse array of strengths that offer opportunities for investors with different needs.

China: China has adopted a robust policy response in answer to fractious economic relations with the US that will deepen existing competitive advantages.

The Chinese government’s newest five-year plan (2021-2025) emphasises cultivating domestic consumption (over exports) and innovation in key strategic technological industries. This should mean continued emphasis on developing already advanced e-commerce and internet platform capabilities. At the same time, the government wishes to develop technology for electric vehicles (EV), as well as 5G to boost the country’s technological base.

Korea: Companies remain leaders in the memory chip and EV and renewable energy storage sectors. We believe these companies will be at the forefront of the development and structural growth trend of migration to 5G technology, EV and renewable energy.

India: We remain optimistic about the outlook of the IT outsourcing and pharmaceutical sectors. These sectors represent India’s core comparative and competitive advantage globally and we believe the demand for their products and services is structural in nature.

Over the longer term, we are closely monitoring the opportunities created by India’s “Make in India” initiatives. India has announced several measures aimed at self-reliance including import disincentives, production-linked incentives, tax benefits and digitisation to increase the share of manufacturing in GDP from 17% currently to 25% over the medium term6.

ASEAN: ASEAN countries are strengthening efforts to attract foreign direct investment and deepen their competitive advantages.

Countries in the region possess different strengths. Thailand has a strong automotive supply chain and a well-established food manufacturing industry. Malaysia possess an advantage in the manufacturing of electronic and electrical products, rubber gloves and wooden furniture. In contrast, the Philippines provides great service in terms of business process outsourcing (BPO) and Indonesia is offering itself as the hub for electric vehicle supply chain. Finally, Vietnam has established a niche in the manufacturing of smartphones and electronic components.

Taiwan: The technology supply chain in Taiwan is expected to continue to play an important in supporting tech innovation in China and the US over the mid-term. The ability of local producers in key industries such as semiconductors to stay ahead of the technology curve has given them a competitive advantage over global rivals. Taiwan has also developed world-class companies in servers, 5G components, and IC design.

Based on this vision for Asia, we see the following four structural themes as critical for investors in 2021:

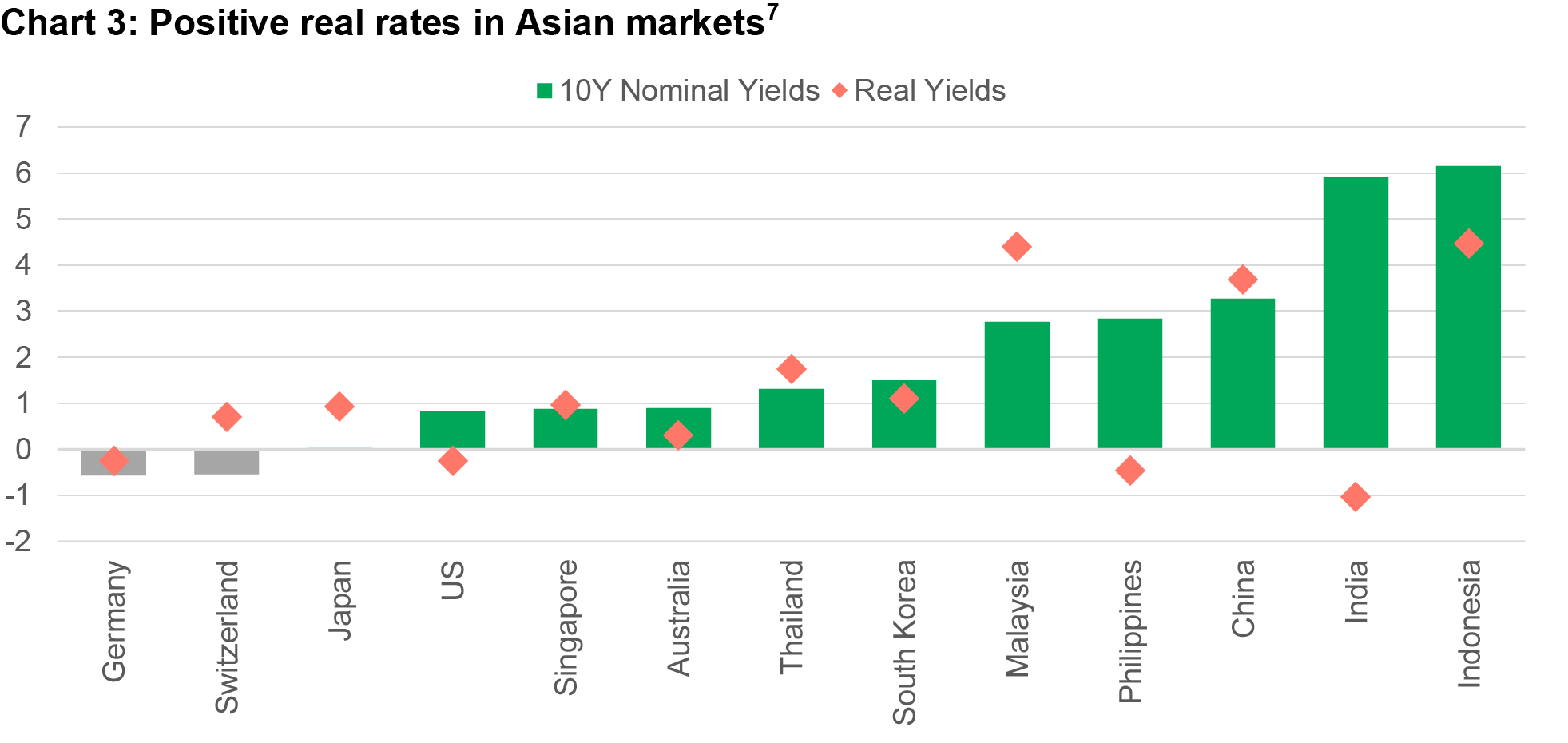

We expect that major central banks will keep interest rates near zero over the short-term. With inflation forecast to be in positive territory, this has and should continue to result in negative real rates and bond yields in many developed markets.

In contrast, many Asian markets currently offer positive real yields (see Chart 3). With a relatively optimistic growth forecast in 2021 for the region, we expect the yield differential between developed markets and Asia to continue in the upcoming year. This dynamic should be constructive for capital inflows in Asian equity markets, as global investors look to capitalize on the region’s robust economic rebound and attractive yields.

5G technology promises to transform the 2020s into a time of unprecedented connectivity and technological advancement, dramatically expanding the reach of Internet of Things (IoT). Indeed, 5G and IoT will enable greater use of connected devices that automate onerous business processes. This includes factory automation: Many manufacturers have announced their plans to automate their factories to overcome the issues of labour shortages and enhance productivity.

We expect broader availability of devices developed with 5G to be launched in the next few years. This is expected to trigger a replacement cycle globally and we believe the supply chain in Asia, particularly the tech supply chain in North Asia (Taiwan, China, Korea) will benefit from this trend.

With the risks of climate change becoming more apparent, countries are adopting ambitious policies to address the problems8. These initiatives, coupled with greater attention to ESG in investment decisions should lead to more climate friendly and sustainable projects, e.g. renewable energy infrastructure and equipment. As a result, we envisage that the development and adoption of electric vehicles and energy efficient products should accelerate and the ecosystem of renewable energy and resources, e.g. energy storage, battery charging stations, energy efficient semiconductors/chips and recyclable materials. Investments in this area is expected significantly grow.

Global supply chains, and China’s role in it, have undergone significant changes due to the global spread of COVID-19 and the fallout from the prolonged Sino-US trade conflict. Some firms may shift production out of China (production relocation) on concerns over the vulnerability of single production location or rising tariffs. Others might choose to diversify customers and redirect exports to other markets (trade redirection) in light of geopolitical risks. South-east Asian countries, particularly Vietnam, have benefited from multinational and Chinese companies relocating or setting up new factories in the region. We expect this trend to continue and governments in South-east Asia have introduced incentives and amended regulations9.

Although parts of Asia have fared better than others after the global shock of COVID-19, the road to recovery (both physical and economic) should remain a key theme of 2021.

For long-term investors, Asia offers the opportunity to not only participate in sustainable growth in world-class companies, but also to achieve diversification through exposure to different industries. Overall, the region’s opportunities add up to more than the sum of its diverse parts.

1 China and Taiwan did not enter technical recession, while Hong Kong and Korea did.

2 Bloomberg, as of 29 December 2020, MSCI Asia (ex-Japan) posted a return of 21.84% (total return in US dollar).

3 Bloomberg, as of 29 December 2020., MSCI Korea was the best performing regional market up roughly 40.30% (total return in US dollar), while MSCI Thailand was the worst performing market declining by 10.79% (total return in US dollar).

4 Bloomberg, as of 15 December 2020.

5 Manulife Investment Management.

6 Goldman Sachs, as of 15 November 2020.

7 Bloomberg, as of 30 November 2020.

8 In a September speech to the United Nations, Chinese President Xi Jinping put a 2060 end date on his country’s contribution to global warming. President-elect Joe Biden has also pledged to re-join the Paris Agreement after being sworn in on 20 Jan 2021.

9 Indonesia recently passed the Omnibus Law in Indonesia, while India passed the Production Linked Incentive in India.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

© 2026 Manulife Investment Management. All rights reserved.