30 May 2019

Increased trade tensions at the beginning of May have frayed nerves and, by extension, market returns. It’s unsurprising, therefore, that equity markets didn’t respond well to being reacquainted with trade-policy uncertainty. Our Asset Allocation Team’s Macro Strategy Team reckons that in times of heightened geopolitical risk, the best way to remain focused on economic fundamentals is to cut through the market noise.

In the US and Europe, incrementally better data has generally reinforced the team’s view that the next few months should be marked by stabilisation and/or improvement. The inflection higher in recent US retail sales data should not only serve to stabilise the US economy over the coming months, but also potentially support global manufacturing impulses. Furthermore, China’s macro outlook has improved given the comprehensive list of monetary and fiscal-stimulus measures. However, the spillover effect on the global economy may not be as extensive as before. As a result, the team thinks it is important to temper optimism around the “it’s time to be bullish about EM Asia” thesis that’s been making the rounds.

April’s market action is perhaps best characterised as being neutral to slightly positive; unfortunately, increased trade tensions at the beginning of May have frayed nerves and, by extension, market returns. Policy uncertainty aside, incrementally better data out of Europe and the United States has generally reinforced our view that the next few months should be marked by stabilisation and/or improvement. In our minds, while progress has been uneven, any inflection higher i n U S retail s ales d ata w ould b e a positive development that should not only serve to stabilise the US economy over the coming months, but should potentially support the global manufacturing impulse as well, which has softened markedly over the last several months.

Our take on recent market action: It’s unsurprising that the equity markets didn’t respond well to being reacquainted with trade policy uncertainty. The hardest hit were emerging markets, which went from being slightly positive to approaching correction territory over last six weeks. While returns were negatively affected across the board, the magnitude has been different1.

Overall, we continue to expect to see better macroeconomic data over the summer, but we’d add that the return of policy uncertainty and strong year-to-date equity market returns could imply a choppier trading environment. At this stage, a more proactive investment approach is likely the best strategy to pursue, especially against a backdrop of potentially slower growth around year end.

China’s extensive list of monetary and fiscal stimulus measures is starting to produce an observable stabilising effect on its economy. After over a year of disappointing Chinese economic data, first-quarter data has beaten market expectations—the latest monthly Purchasing Managers’ Indexes (PMIs) reflect an economy that’s expanding marginally, and most credit data appears to have troughed2. As a result, we’re cautiously optimistic on the Chinese growth story as we expect the economy to continue to stabilise; however, we’re not expecting a substantial v-shaped recovery like the one seen in 2015/2016.

Traditionally, an improvement in the China outlook implies important positive spillover effects to the global economy, particularly emerging markets (EMs) in Asia. In our view, the effects are likely to be more limited this time around, and with longer lags than what we’ve seen in the past. As a result, we think it’s important to temper optimism around the “it’s time to be bullish about EM Asia” thesis that’s been making the rounds.

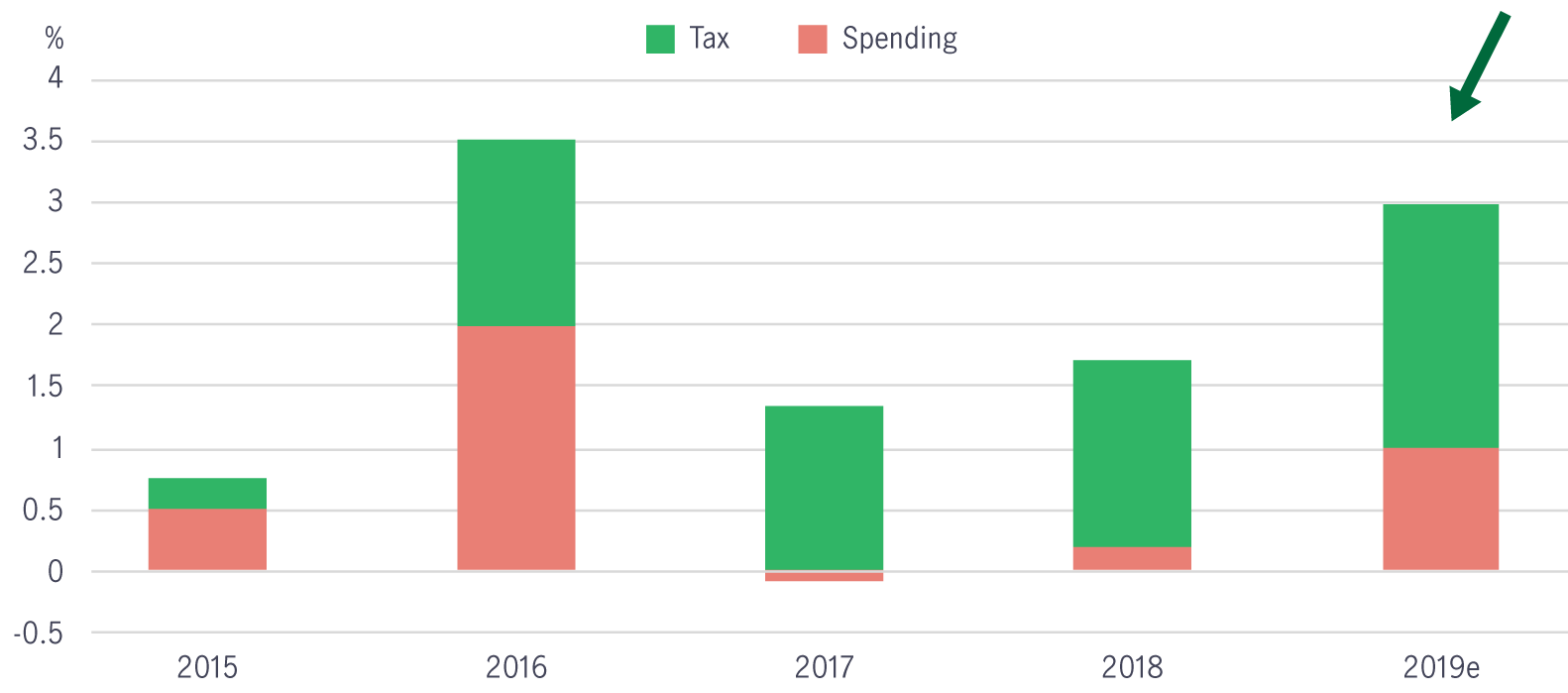

By many measures, China’s current round of fiscal and monetary stimulus is as massive as what it had introduced in 2015/2016, yet its composition is substantially different (see chart 1). Over the past year, China’s fiscal stimulus has been predominantly focused on domestic consumption; for instance, authorities announced the country’s largest ever personal income-tax cut, which has boosted middleclass incomes. This is in stark contrast to previous rounds of stimulus that focused on the property sector—the most commodity-intensive sector—and infrastructure projects, which created demand for intermediary goods, commodities, and external goods.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Latest asset allocation views for Asia Q1 2026

Three key global themes for the first quarter: Liquidity and stimulus set the stage for 2026; AI remains a structural growth driver; Accelerating growth may favour diversification

Source: Thomson Reuters, Manulife Asset Management, 17 May 2019. 2019e refers to estimate.

While the current round of stimulus is certainly powerful enough to lift the Chinese economy, its domestic nature implies that it’s less likely to lead to the marked increase in international trade activity than we’ve witnessed in the past. Global trade is typically the default channel through which the Chinese recovery is filtered through to the rest of the world; without a sizable improvement in Chinese import volumes, China’s stabilisation is likely to benefit its trading partners to a lesser degree.

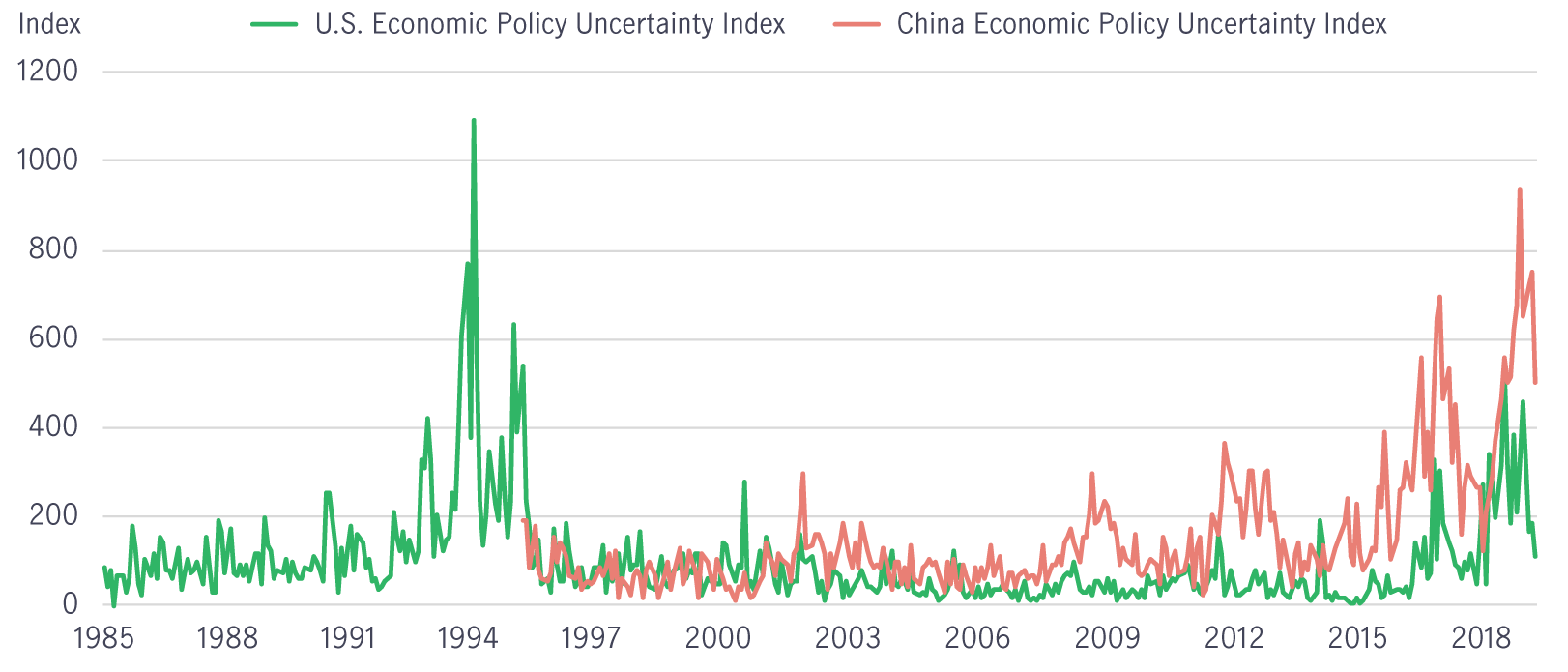

Source: Thomson Reuters, 17 May 2019.

Critically, heightened uncertainty over US-China trade relations will almost certainly compound weak trade activity in the region, particularly in light of the fact that China’s consumption-targeted stimulus is likely to be more sensitive to confidence channels. It’s also possible that worsening trade negotiations could amplify the odds of additional stimulus from Beijing policymakers, but we believe any forthcoming measures are likely to be similar in nature to those that are already announced.

Despite expectations for a more muted impact, it’s still reasonable to assume that global trade volumes will improve marginally as China’s economy stabilises. Even then, we don’t expect an immediate rebound in EM growth—several EM Asian economies, including Taiwan and South Korea (Chart 3), have elevated inventory levels that will have to be worked through before they can raise production. This wasn’t the case in 2015/2016, which in turn suggests a potentially longer lead time for real economic growth in EM Asia to rebound after trade channels have been reawakened.

Source: Bloomberg, TD Securities

In 2015/2016, several EM economies benefited from higher commodity prices following significant supply-side cuts from China’s heavy industry sectors (such as coal and steel), which included production and capacity cuts. These cuts resulted in higher capacity utilisation rates that pushed the prices of these commodities higher and boosted profits in these sectors. This time around, however, the opposite occurred—the relaxation of some production cuts has kept key commodity prices relatively contained. As a result, economies in EM Asia that typically benefit from higher commodity prices may not get that much of a lift from China’s current stimulus.

Finally, USD resilience has become an additional headwind for EM Asian economies—their import costs rise as their currencies weaken against the greenback. We expect the USD to remain supported by better US growth and heightened geopolitical risks over the next quarter, effectively placing a cap on growth in EM Asia.

In times of heightened geopolitical risk, we often suggest focusing on economic fundamentals in an effort to cut through the noise. For the United States, however, the fundamentals don’t look as positive as they did a month ago. First, we believe most of the positive US macroeconomic news (healthy growth and muted inflation) was priced into equity markets in April, meaning we’ll need another positive catalyst, such as strong earnings or improvements in European data, to continue to grind higher. Those positive catalysts have yet to—but may not—materialise. Second, we’re now slightly less positive on Q2 US growth after Q1 GDP data showed a sizable buildup of inventories. This suggests that Q2 inventories will have to unwind, which tends to drag on growth data. Third, there have been multiple instances in which business investment both in the United States and abroad stalled during periods of heightened uncertainty; we expect corporate confidence to fall as a result. In summary, while we maintain a positive outlook on growth over the summer, we’re also expecting more volatility in equity markets. US interest rates are likely to stay at current levels, as the US Federal Reserve is likely to double down on its wait-and-see approach to its interestrate policy.

Source: Manulife Asset Management, as of 14 May 2019.

1 Bloomberg, 28 May 2019. MSCI Emerging Markets index posted a 2.00% gain in April 2019, while it corrected by 6.05% from 1 April 2019 to 20 May 2019. Price returns in US dollar.

2 Bloomberg, 28 May 2019.

© 2026 Manulife Investment Management. All rights reserved.