When it comes to managing household finances, budgeting makes sense. However, it’s sometimes hard to accurately estimate what your outgoings will be each month. Unexpected bills and one-off costs can disrupt the best-laid plans! While there is no perfect way to ensure you live within your means, we have some suggestions that might help.

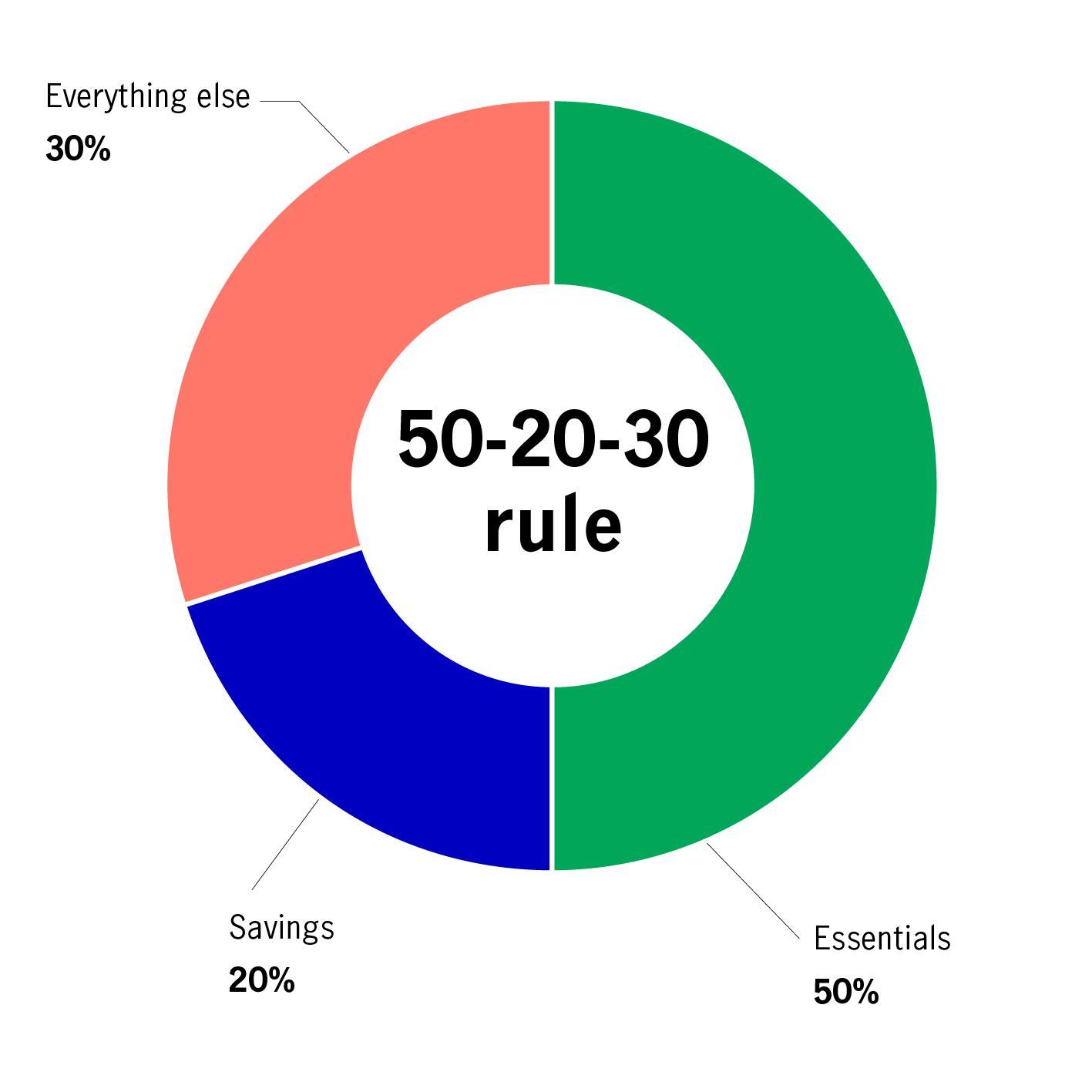

First of all, there’s the 50-20-30 rule. A wealth-management technique that divides your monthly income into three categories:

50% for essentials: rent and other housing costs, such as groceries, electricity or transport

20% for savings: savings accounts, retirement contributions, loans, or credit card payments

30% for everything else: non-essential expenses, such as clothing, eating out, monthly streaming subscriptions, or gym memberships

While you might not have a problem remembering the numbers 50-20-30, the rule itself isn’t always easy to live by. When it comes to expenses, one size doesn’t fit all and lifestyles will vary depending on, for example, where you live. City living can be more expensive and people may spend a large part of their income on rent, which can cause problems if your income is irregular. Housing costs can also be particularly tough for those in low-paid jobs.

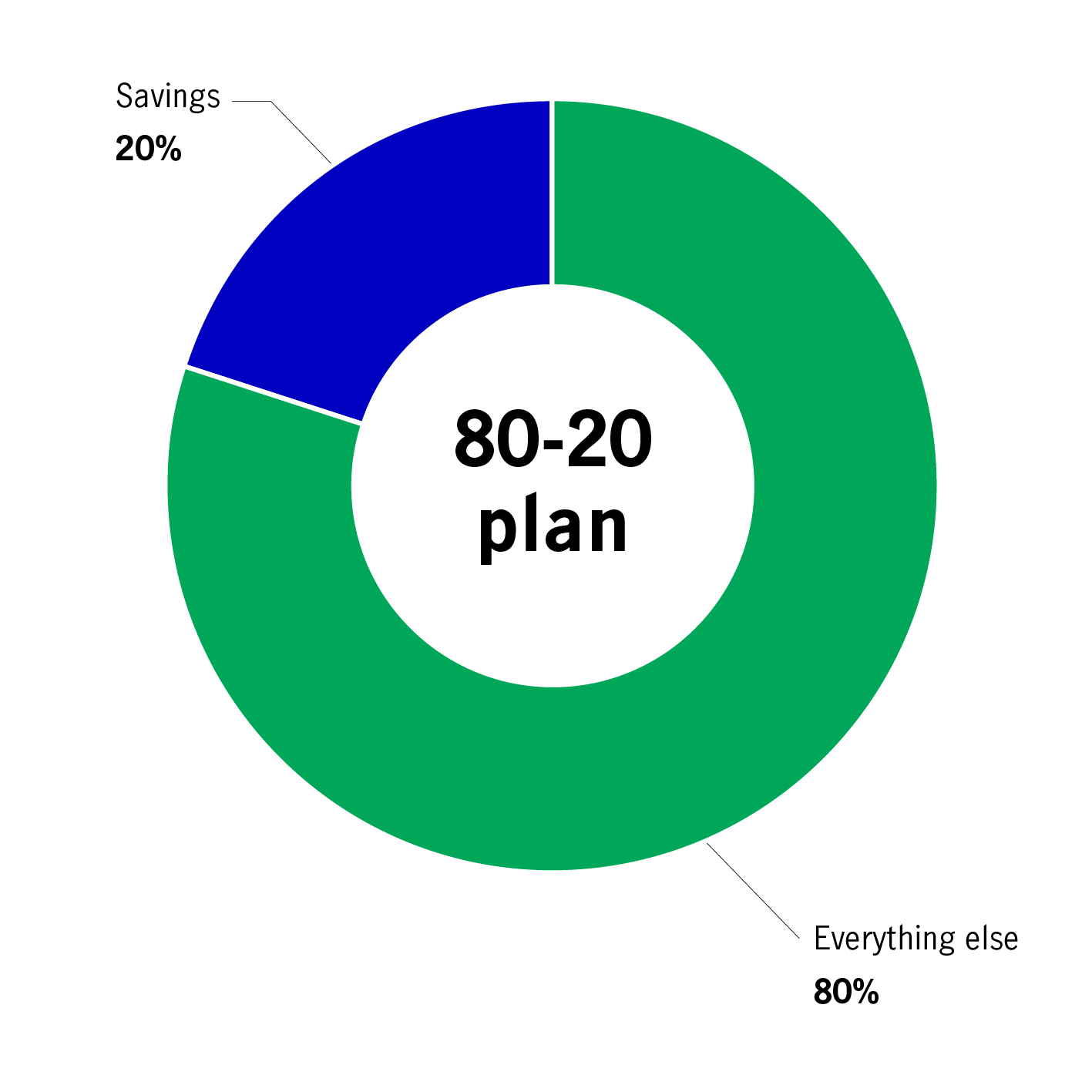

Even simpler than the 50-20-30 rule is the 80-20 plan. Instead of separating every expense into what’s essential and what’s not, you take 20% of your monthly income and deposit it directly into a savings account. What’s left over is available to spend however you want.

A good tip here: create an automatic transfer that sets aside 20% as soon your monthly salary is paid. By immediately placing the cash in a separate savings account, it’s like you never had it in the first place!

Everyone’s budgeting needs are different. That’s why it’s sometimes better to create your own method. Start by calculating all your monthly expenses. Check your bank statements to make sure you’re noting everything down. Mortgage or rent costs are easy to remember, but subscriptions, such as streaming services or phone contracts, may slip through unnoticed. And remember to account for payments that come off less regularly, such as annual fees.

Once you know how much you spend, a quick calculation will tell you what’s left each month. This is easy when you have a regular salary but could be a little harder to determine if you have a freelance job or get extra funds from other work, rental income, or interest payments.

Quick Budgeting Checklist:

Once you’ve counted up all these numbers, you can decide where your money will go each month and how much disposable cash remains.

Remember, it’s important to monitor your expenses on an ongoing basis. Save all your receipts and cross check them against your card statements at the end of the month. See if you’re overspending in certain areas or if you can save a little more.

Keeping an eye on income and spending is not easy. However, working to a budget can simplify matters. Once you have established a reliable system that tracks your money, the process becomes less tricky, and you’ll find it easier to take control of your finances.

Source: John Hancock

How much do I need to save?

Find out more by using our target savings calculator!

Beyond the Hyperbole: Three Macro Takeaways from the 2024 US Elections

What investors and policy watchers should take away from the 2024 election results depends, in part, on time horizon.

How might the US election and China’s stimulus package impact Asian fixed income?

Asia Fixed Income Team analyses how the US election and other recent major events could impact the region’s fixed income markets.

How to Protect Yourself and Your Accounts Online

Technology has enabled us to live with convenience and accessibility more and more each day. We have great power at our fingertips and can effortlessly perform numerous tasks from our phones and laptops, including managing our finances online. However, as we grow more adept at using these apps and tools, and as technology evolves and becomes increasingly sophisticated, we must continually educate ourselves on how to safeguard our data and security,and avoid becoming targets of cybercriminals.

How to Protect Yourself and Your Accounts Online

Technology has enabled us to live with convenience and accessibility more and more each day. We have great power at our fingertips and can effortlessly perform numerous tasks from our phones and laptops, including managing our finances online. However, as we grow more adept at using these apps and tools, and as technology evolves and becomes increasingly sophisticated, we must continually educate ourselves on how to safeguard our data and security,and avoid becoming targets of cybercriminals.

Manage your expenses but don’t forget retirement planning

By the time you hit 30, the cost of hosting a wedding, having kids, and buying property should not be taken lightly. It’s worth adhering to the three principles of wealth management.

Investing when markets are volatile – How markets fared a year since the pandemic

In 2020, we released our first edition of the “Investing When Markets Are Volatile” series, where we discussed three lessons from history that all investors should know about market volatility.

© 2026 Manulife Investment Management. All rights reserved.