27 April, 2020

In this market note, Sue Trinh, Senior Macro Strategist, Manulife Investment Management, examines the immediate impact of COVID-19 on markets in Southeast Asia. She also assesses the potential longer-term effects of the outbreak on the region's economies. Particular attention is paid to GDP growth in Indonesia, India, and the Philippines.

The COVID-19 outbreak is affecting Asian economies through many direct and indirect channels. In summary:

As with most things in markets, any investment thesis depends on the investment horizon.

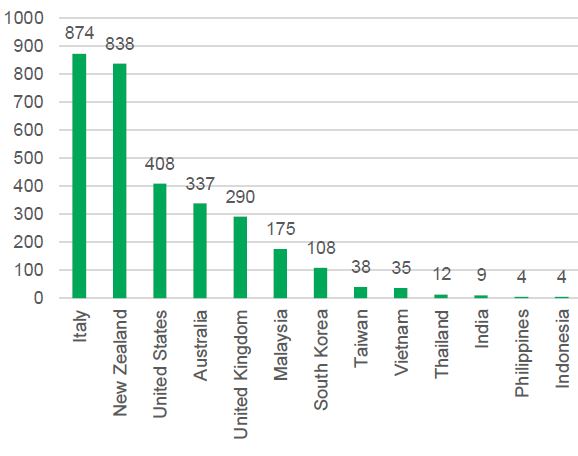

In the short term, the market may turn its attention to those economies that could become the next COVID-19 hot spots. Worryingly, there have been rapid increases in the confirmed cases reported in Indonesia, India and the Philippines – these are the region’s more populous economies with a more significant share of its low-income households, thinner social-security nets and weaker health infrastructure. These markets have also recorded a higher proportion of deaths, which suggests that the actual number of virus-related infections could be greater than reported due to their lower testing capacity (a function of health infrastructure).

Source: National Sources, Manulife Investment Management, as of 8 April, 2020.

If we look at the longer-term picture, many independent issues have been exacerbated by COVID-19. For instance, a protectionist push is now accelerating across the world, the US dollar is much stronger, and oil-price volatility is creating deflationary pressures, which has implications for credit markets and financial stability. Therefore, rather than a mechanical application of first in, first out, we need a more holistic approach when assessing the potential longer-term economic impact in the region.

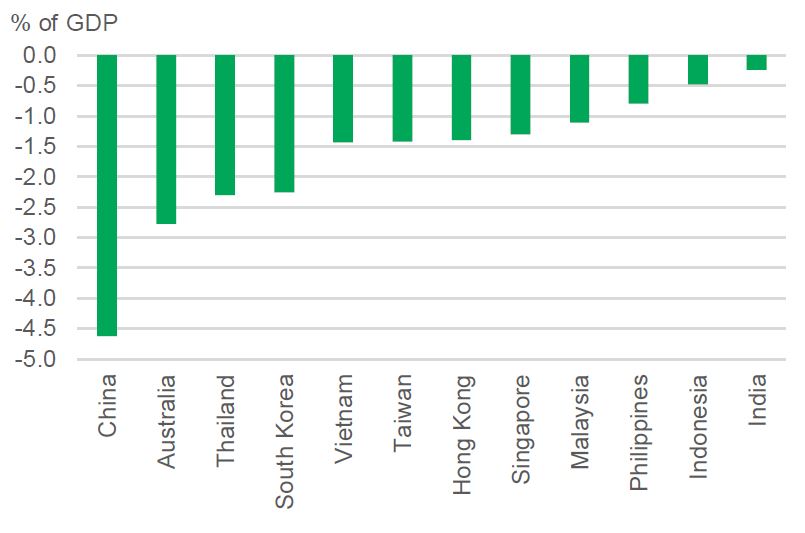

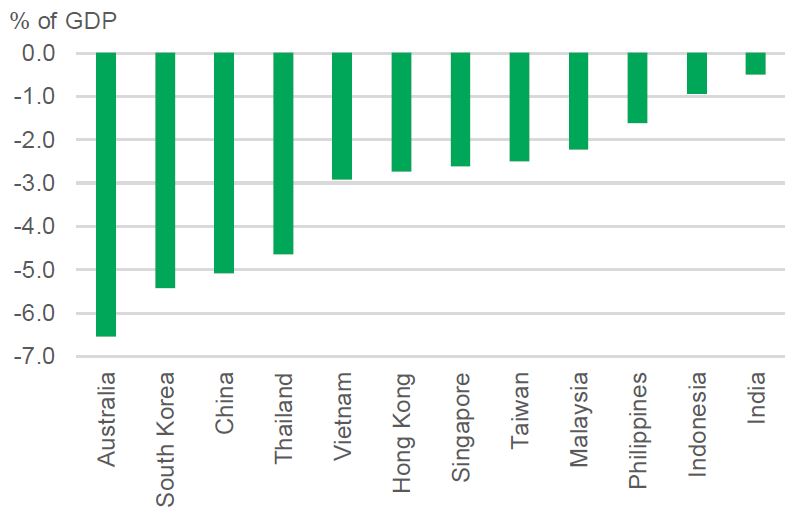

Such a view would take into consideration the quality of health infrastructure, testing capacity and fiscal wherewithal of an economy, along with its ability to pivot supply chains and grow domestic demand. Credit and liquidity risk exposures will also be pertinent. While Indonesia, India, and the Philippines may face the near-term risk of local outbreaks, their economies are among the most insulated from a longer-term growth perspective. Indeed, the Asian Development Bank's recent scenario analysis (chart 2 & 3) indicates that these markets are likely to experience the lowest impact on GDP growth, regardless of timescale.

Source: ADB, Manulife Investment Management, as of 8 April, 2020.

Source: ADB, Manulife Investment Management, as of 8 April, 2020.

Near-term newsflow may be negative, particularly as these markets deal with domestic outbreaks. However, the impact of the COVID-19 must also be viewed in a longer-term context. To this end, we believe Southeast Asia should emerge from the pandemic with resiliency.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Latest asset allocation views for Asia Q1 2026

Three key global themes for the first quarter: Liquidity and stimulus set the stage for 2026; AI remains a structural growth driver; Accelerating growth may favour diversification

© 2026 Manulife Investment Management. All rights reserved.