27 May 2022

How much savings do you think is sufficient for retirement? PHP 10 million? PHP 20 million? To live comfortably in silver age, your goal should not be merely to accumulate assets worth a nominal value. Inflation should also be considered to ensure an investment appreciates over the years, so its real purchasing power can satisfy your retirement needs. If an investment strategy is too conservative, the principal could be preserved at retirement, but its purchasing power may be eroded by inflation.

The destructive effects of inflation should not be underestimated, as even a slight increase (which compounded over the years) can lead to a heavy burden in retirement. However, its actual impact depends on changes in expected inflation and age. In simple terms, younger people are affected more because they are further away from retirement age, which means high inflation erodes their purchasing power over a longer period.

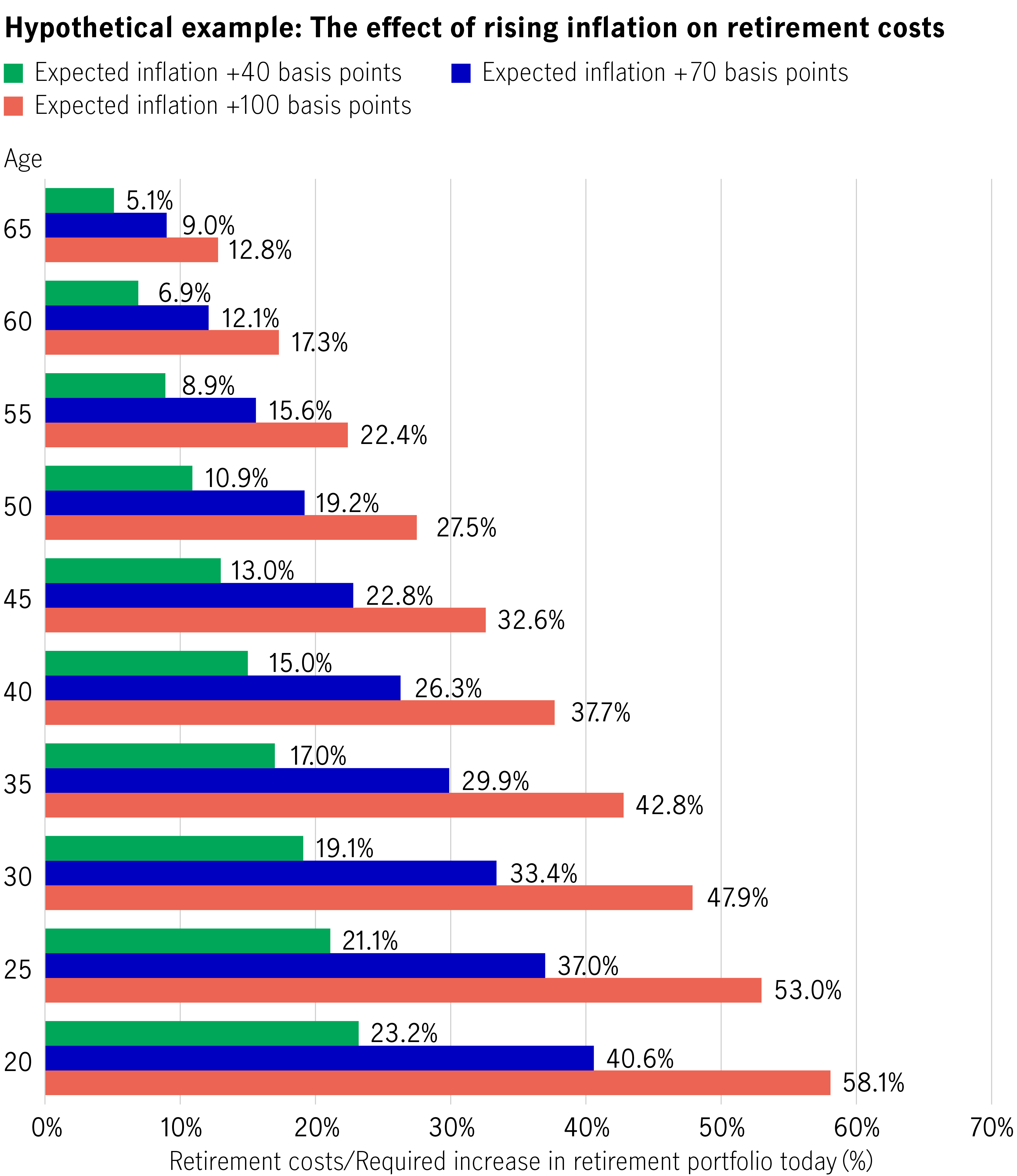

According to Manulife Investment Management’s calculations, suppose there are three investors aged 25, 45, and 65, respectively, who all retire at age 65 and have the same annual expected expenses after retirement. We found that:

Looking at it from another perspective, the three individuals must immediately increase the corresponding amount of savings/wealth in their retirement portfolios (i.e., increase their savings) to offset the effects of inflation so that they can withdraw the predetermined amount of real income (i.e., inflation adjusted) each year according to plan.

Manulife Investment Management calculations, as of 1 February 2022.

It is, of course, not easy to inject a large lump sum into your retirement portfolio. If investors do not have spare or ready cash or choose to ignore inflation, the purchasing power of their assets will be heavily discounted in the future.

For example, if price levels rise at 2% per year, and the investment return is assumed to be 0% (holding cash and not making investments) and 1% (lower risk assets with an annual return lower than inflation) each year, real purchasing power (inflation-adjusted purchasing power of assets) after 35 years will be 50% and 29% less, respectively!

If the investment return rises to 2% each year, which is equal to the inflation rate, real purchasing power will remain the same throughout the investment period until retirement. Suppose the expected investment return rises further to 5% each year – in that case, your real purchasing power will increase continuously as the return is higher than inflation, and you will have gained 176% by retirement (see the following hypothetical example).

Assumptions:

Example for illustration only.

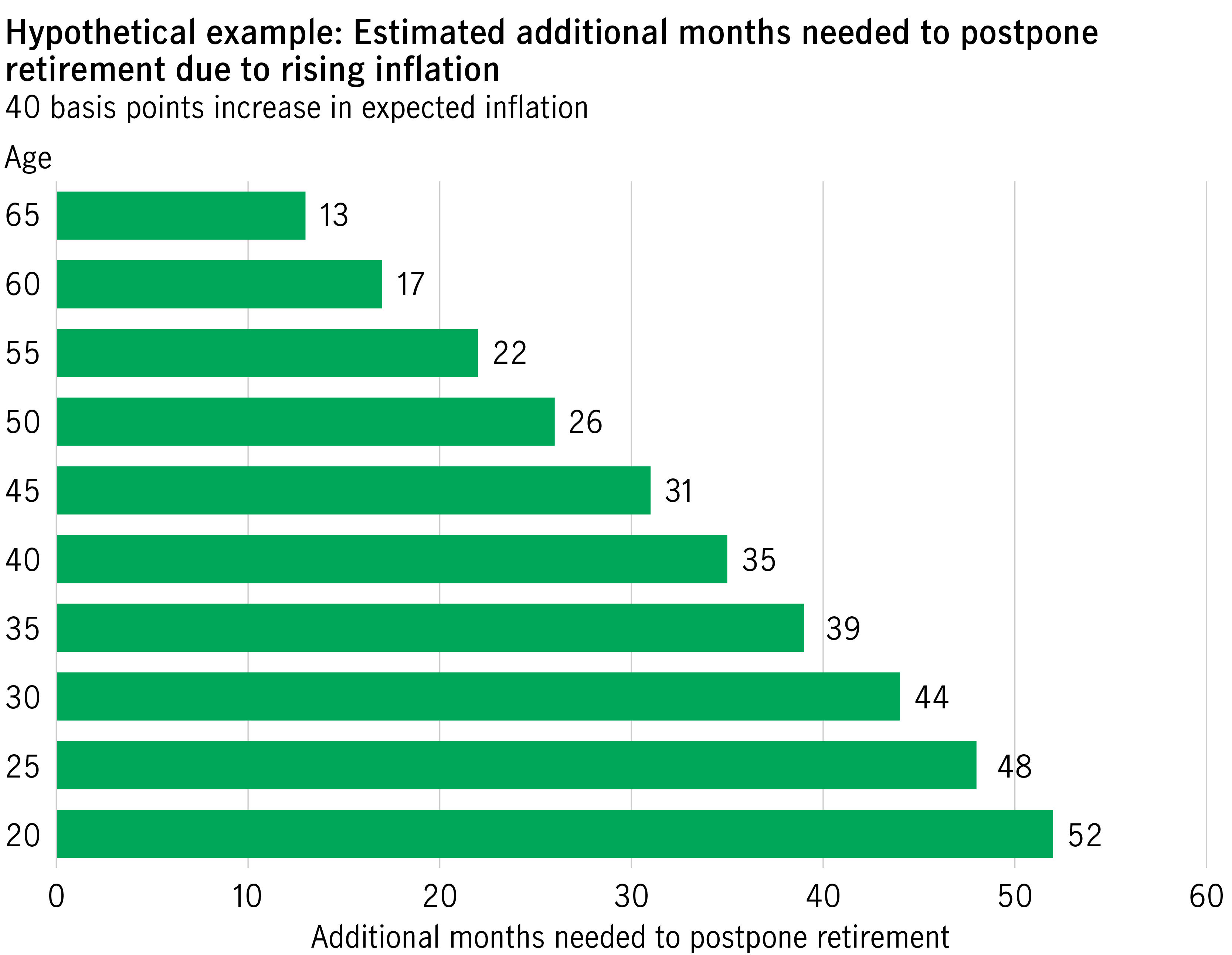

With inflation on the rise, if investors cannot inject more savings/funds into their portfolios but wish to avoid eroding their real purchasing power, they can consider postponing retirement.

Manulife Investment Management calculations, as of February 1, 2022.

In the example above, if expected inflation rises by 40 bps, investors at ages 25, 45, and 65 would have to postpone retirement by 48, 31, and 13 months, respectively, to accumulate enough savings to cover their post-retirement expenses.

No one can control the rise and fall of inflation or accurately predict how prices will rise in the future. Investors should understand the effects of rising inflation on retirement costs and plan according to the above examples. Therefore, it is crucial to consider inflation when planning for retirement. The growing rate of an investment portfolio (portfolio return) should keep up with or even exceed inflation. As young investors will not be retiring soon, they can tolerate a higher level of risk. Therefore, their portfolios may focus on assets with a greater potential return, such as equity funds and bond funds.

1. Manulife Investment Management calculations, as of 1 February, 2022. This is a hypothetical mathematical illustration only. This is under certain assumptions about real interest rates and asset class returns of the multi-asset solutions team. Figures are based on assumptions as set out, and individual circumstances and objectives may vary.

Risk Diversification

There is no free lunch. But Risk Diversification comes close in investing. A diversified portfolio was shown to optimize returns with lower volatility in the long run.

Disadvantages of fixed deposit: is fixed income a better option?

What is a Fixed Deposit? What is Fixed Income? We explain why is fixed income now a potentially better option than fixed deposits.

Seven questions about dividends

Dividends can be a significant source of returns for equity investors. What are dividends? How do dividends fit into portfolio construction?

What does short-term oil price volatility mean for pension scheme members?

Recent geopolitical tensions involving Iran have renewed focus on oil prices and their potential economic and market effects. How can retirement savers navigate short term oil price volatility?

More years, better living

They say that 60 is the new 50, so if you are nearing the next chapter of life, why not make the most out of your golden years by embracing new experiences, pursuing passions and enjoying life to the fullest?

Harness lower-risk funds to navigate uncertainty and volatility

Market uncertainties are accelerating recently, this article will discuss how employees navigate the turbulent conditions by making good use of lower-risk fund

© 2026 Manulife Investment Management. All rights reserved.