24 June 2022

Most of us dream about receiving a regular and consistent stream of income during our retirement years. But how achievable is this goal? The truth is, even if you do not enjoy the benefits of a well-funded employer pension scheme, such as those offered by the civil service, you can still enjoy an income with a prudent investment plan.

There are various types of payout strategies after retirement. Before selecting the investment vehicle that suits you best, consider the following factors:

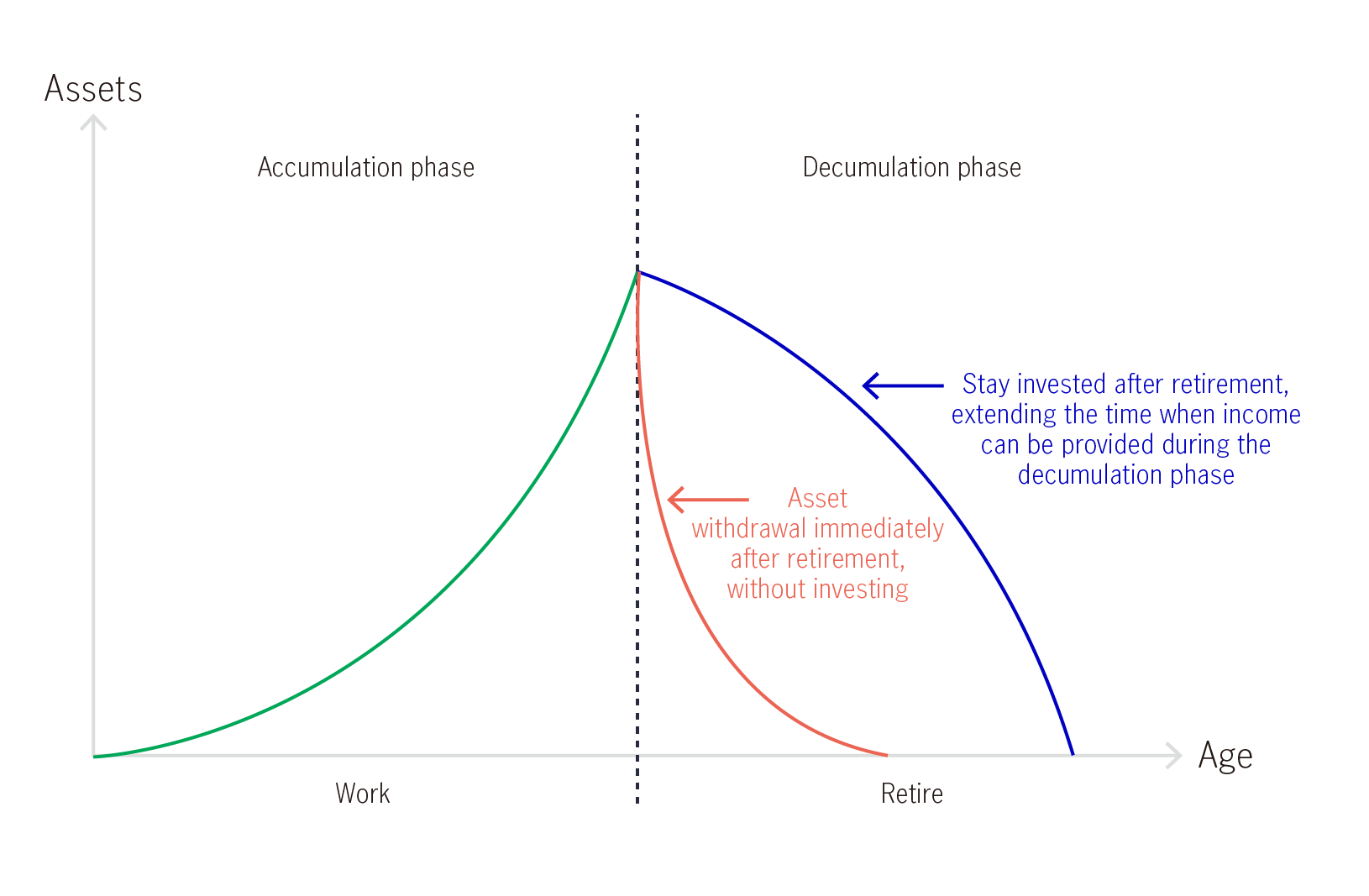

Let’s talk about the MPF first, which people do not immediately associate with regular income payments. Under normal circumstances, employees must wait until they reach 65 before withdrawing their mandatory and tax-deductible voluntary MPF contributions. While there is a legal age limit before you can withdraw from the MPF, it is not compulsory for those who have reached 65 to empty their MPF accounts.

In other words, the operation of MPF accounts is not directly related to the age of employees. If there are no special funding needs after retirement, employees can choose to keep the account and postpone withdrawal beyond age 65. This allows the funds in the account to remain invested and take advantage of potential capital appreciation and/or income opportunities.

Retirees with no employment income may be better suited to investments that generate monthly income (cashflow). Some MPF trustees and fund companies currently offer income funds with a monthly dividend distribution feature. The share class of some retail funds withdraw from the principal to make monthly distributions and enhance the overall dividend rate.

If you belong to the fortunate group of landlords who do not have to deal with rogue tenants, then you will receive regular rental payments. As such, buying a property and leasing it to a tenant can indeed yield monthly payouts. Of course, before entering into any investment, you are encouraged to do your homework, as taxes relating to rental income may significantly undermine the actual payment. Furthermore, real estate as an asset is relatively less liquid, implying that you may not be able to quickly generate cash for a rainy day.

Two other popular payout tools include equities (such as the high-dividend stocks with robust businesses) and bonds (such as government bonds or inflation-linked bonds). However, both are more liquid, with dividends usually paid quarterly or semi-annually. Therefore it might not suit those retirees looking for monthly funds.

In addition, retirees have to bear higher concentration risk when investing in a single stock or bond, as issuers may be unable to deliver payouts due to different factors, such as financial conditions or regulatory authorities’ requests. Comparatively speaking, a fund contains a basket of holdings, offering better risk diversification while enjoying liquidity benefits similar to equities.

It should be noted that investment vehicles offering payouts do not only appeal to retirees, they are also suitable for those investors waiting for the right opportunity to realise specific financial goals and can utilise idle cash through active, flexible asset allocation for some income.

Risk Diversification

There is no free lunch. But Risk Diversification comes close in investing. A diversified portfolio was shown to optimize returns with lower volatility in the long run.

Disadvantages of fixed deposit: is fixed income a better option?

What is a Fixed Deposit? What is Fixed Income? We explain why is fixed income now a potentially better option than fixed deposits.

Seven questions about dividends

Dividends can be a significant source of returns for equity investors. What are dividends? How do dividends fit into portfolio construction?

What does short-term oil price volatility mean for pension scheme members?

Recent geopolitical tensions involving Iran have renewed focus on oil prices and their potential economic and market effects. How can retirement savers navigate short term oil price volatility?

More years, better living

They say that 60 is the new 50, so if you are nearing the next chapter of life, why not make the most out of your golden years by embracing new experiences, pursuing passions and enjoying life to the fullest?

Harness lower-risk funds to navigate uncertainty and volatility

Market uncertainties are accelerating recently, this article will discuss how employees navigate the turbulent conditions by making good use of lower-risk fund

© 2026 Manulife Investment Management. All rights reserved.