11 May 2022

With contributions from the Asian Fixed Income, China Fixed Income, Singapore Fixed Income, Taiwan Fixed Income, and Malaysia Fixed Income Teams. Additional inputs from the India, Malaysia, Indonesian Investment Specialist Team and Philippine Equity Teams.

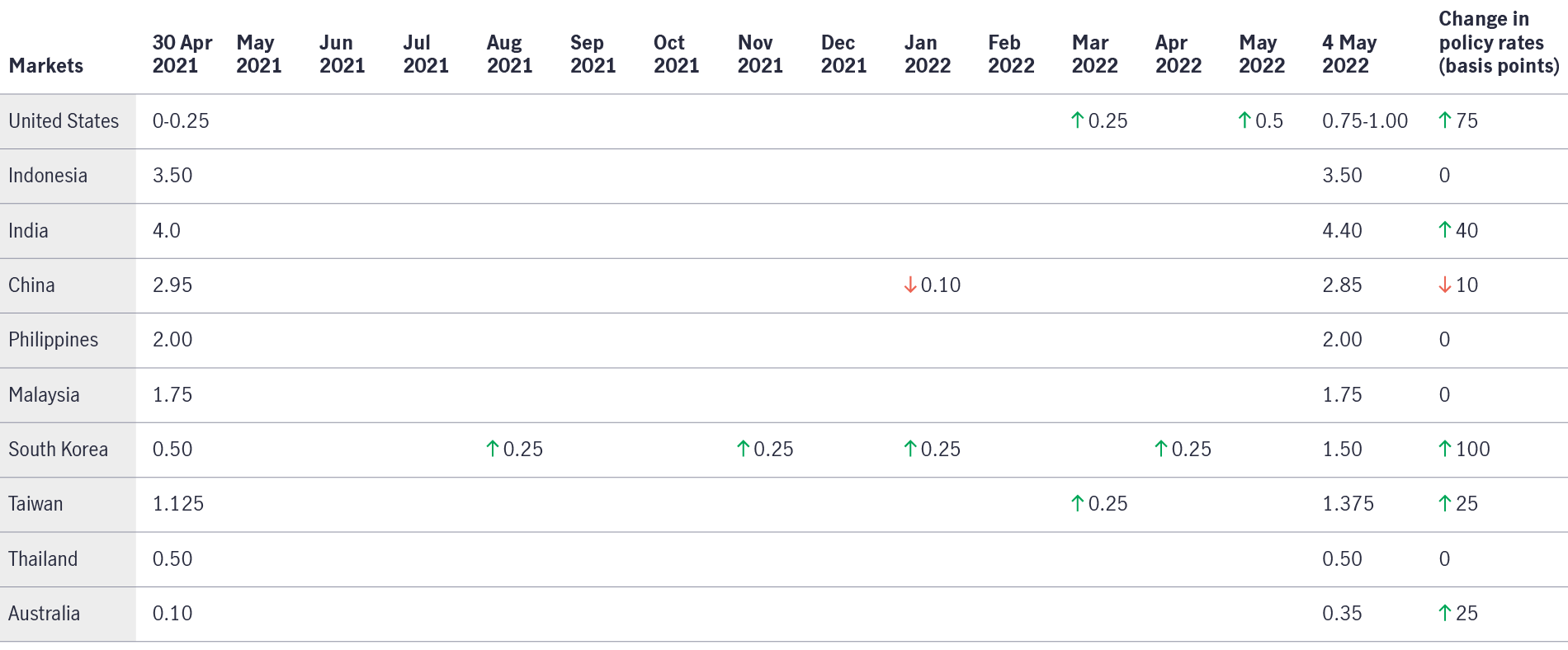

Global central banks started to hike interest rates in 2021, with the US Federal Reserve (Fed) following suit this year. Meanwhile, rate rises across Asia have been more gradual, mainly due to a relatively benign inflationary outlook. In this Investment Note, we draw insights from our pan-Asia fixed income and equity teams, who examine the impact of US-dollar strength and what this means for currencies in the region.

The region’s currencies – a granular outlook

Conclusion

US-dollar strength, a hawkish Fed, and slowing growth in China should continue to place pressure on Asian currencies through the summer months. Even though the region’s central banks are expected to normalise monetary policy, this will be at a slower rate than developed markets. More positively, the outlook for the second half of the year is relatively upbeat.

1 The Bank of Korea has already increased its policy rate by 75 basis points (bps) so far this year, while on 3 May, the RBA hiked the official cash rate by 25 bps to 0.35%, from a record low 0.10%, with the central bank signalling the likelihood of more increases in the coming months. Australian consumer prices rose 5.1% on year in the first quarter, with core inflation rising 3.7%.

2 In the last six months, MAS moved to raise the slope of the band twice amid rising inflation, including an off cycle move in January 2022.

3 Note that in terms of consensus estimates, current account deficit is estimated to remain elevated in 2022 to 2023. Meanwhile consensus estimates point towards a depreciating PHP until 2024.

Key takeaways from Chinese mainland NPC meeting

The annual meeting of Chinese mainland’s National People’s Congress (NPC) is concluding this week. The China equity team shares its latest views on key policy developments and analyses the main growth engines supporting high quality growth.

Latest asset allocation views amid latest Middle East developments

Against a backdrop of elevated uncertainty, the Multi Asset Strategy Team (MAST) summarizes key market moves, and the potential cross-asset implications.

Latest asset allocation views for Asia Q1 2026

Three key global themes for the first quarter: Liquidity and stimulus set the stage for 2026; AI remains a structural growth driver; Accelerating growth may favour diversification

© 2026 Manulife Investment Management. All rights reserved.