12 January 2023

Kai Kong Chay, Senior Portfolio Manager, Greater China Equities

It has been an eventful year for Greater China stock markets, with domestic and global events triggering broad-based weakness and elevated volatility in Mainland China (China), Hong Kong, and Taiwan. In this 2023 outlook, Kai Kong Chay, Senior Portfolio Manager, Greater China Equities and the Greater China Equities team describe the 3 Ps that set the tone for the new year: pivots, positioning and pace forward.

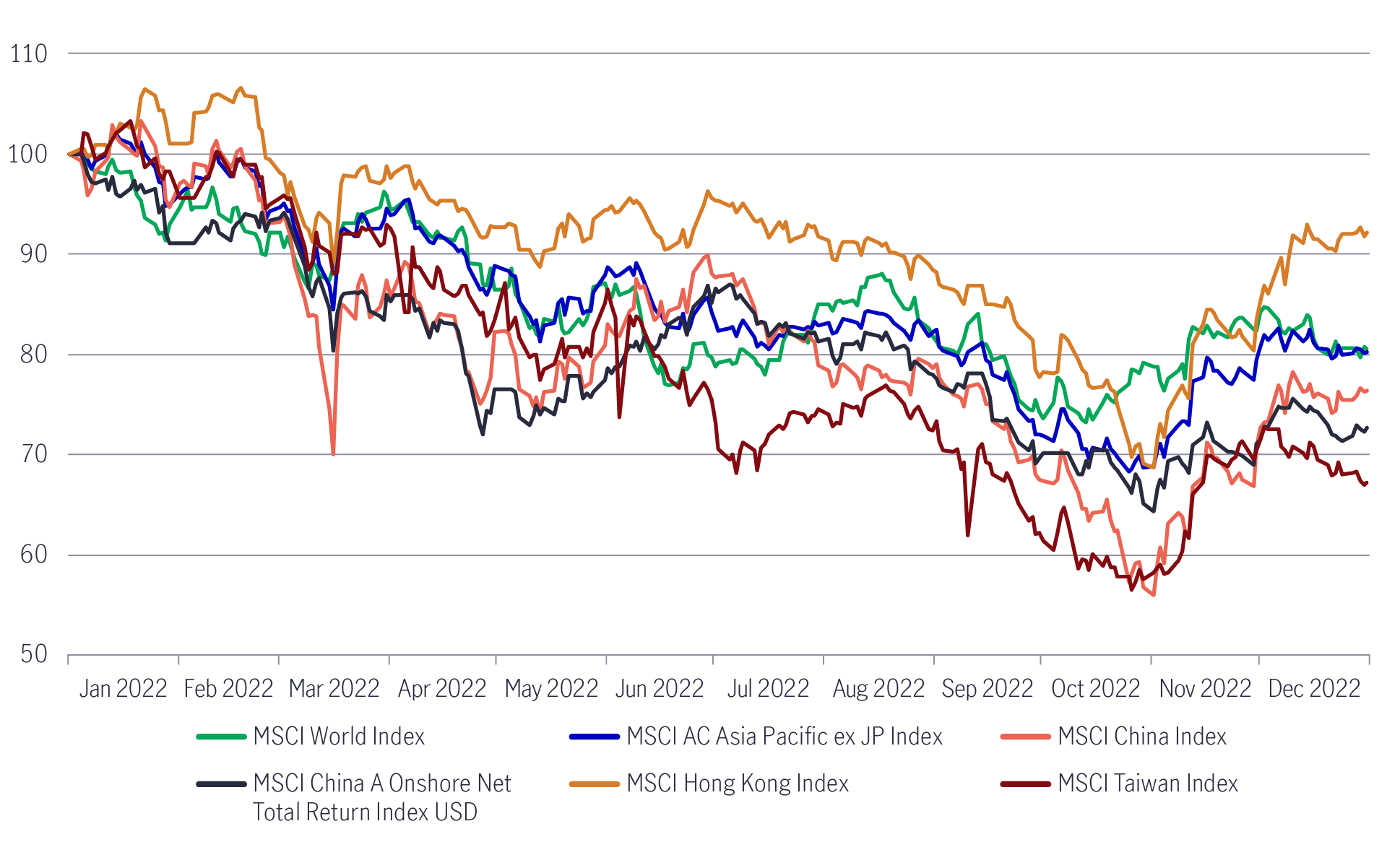

Greater China equities witnessed widespread weakness during the first three quarters of last year on the back of a hawkish US Federal Reserve (Fed), rising geopolitical tensions, as well as COVID-related lockdowns and other restrictions. Taiwan equities were under pressure, as weak consumer demand for electronic mobile devices led to reduced production and inventory build-up in the technology supply chain. Towards the fourth quarter, China pivoted to supportive measures for the property sector1 and the much-anticipated easing of most COVID restrictions, setting the stage for an impressive rally (see Appendix2).

In the next section, we detail our thoughts for the 2023 outlook based on recent pivots and positioning.

We believe that policy pivots and resets matter the most for Greater China equities:

China reopened its border on 8 January 2023, marking the end of a three-year strict-quarantine requirement. Meanwhile, the Hong Kong-China border also reopened.

With the country no longer pursuing zero-COVID, we see a likely reconnection and revitalisation of economic activity (e.g., investment and consumption). This will be crucial for containing logistical disruptions and global inflationary pressures. In our view, China’s GDP is coming from a low base due to the COVID lockdowns – 2023 GDP is looking to be set at 5% or higher. We also expect the economic recovery to start from the second quarter of 2023 onwards, with corporate earnings bottoming out in the first quarter or first half of this year. Thereafter, we might see healthier fundamentals and upward earnings revisions push the market higher. In the near term, we believe that economic data and fundamentals will remain challenging, and earnings might still face pressure.

In November, the People’s Bank of China (PBoC) and other top regulators jointly announced “three arrows” to provide credit, bond, and equity financing support to China’s onshore property developers (both public and private developers). Furthermore, on 5 January 2023, the PBoC and the China Banking and Insurance Regulatory Commission (CBRIRC) jointly announced that the floor on mortgage rates could be lowered or abolished for first-time house buyers in those cities where new house-sale prices had monthly or yearly decline for three straight months. We expect China’s domestic property sales to recover gradually.

The Xi-Biden meeting at the G20 summit brought about a better relationship between the world’s two largest economies3. Facilitated by China’s re-opening, US Secretary of State Antony Blinken is scheduled to visit China in early 2023. Should China and the US resume more bilateral communications, we expect improvements in the market-risk premium to enhance the return upside in 2023.

China’s reopening derives some bright spots for Greater China equities. We believe the following sectors will benefit from China’s reopening, starting from the first-order and second-order derivatives:

1. Re-opening plays

In the wake of China’s reopening, the service recovery should be significant, especially related to travel services and catering. We should see better growth recovery in online travel agencies (OTAs), considering they are scalable and less constrained by raw-material costs, human-resource challenges, and capacity issues. Furthermore, online/e-commerce, food and beverage, catering, etc., could also recover significantly, enjoying stronger tailwinds from fewer lockdowns.

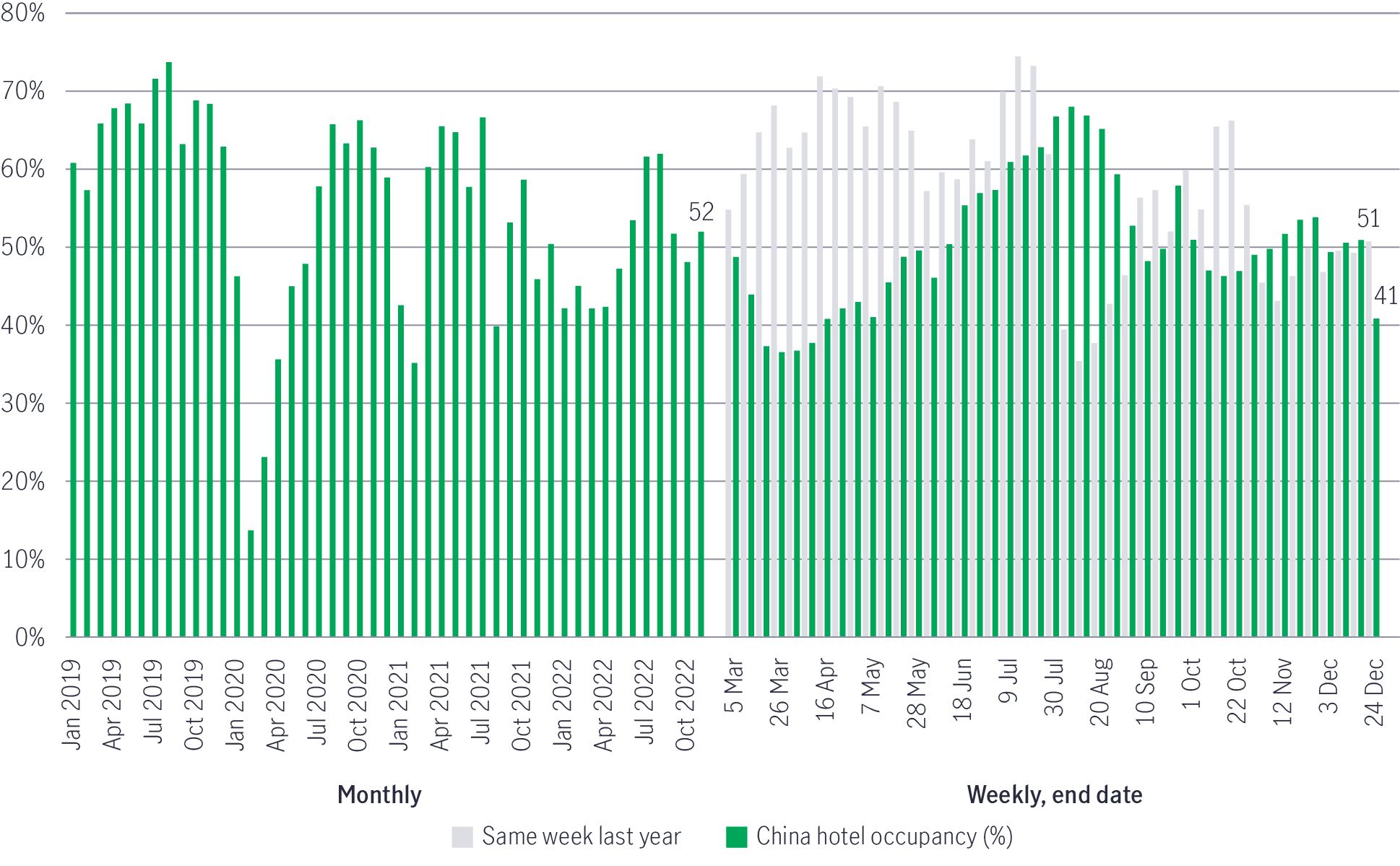

Despite the pullback in hotel occupancies across China in December 2022 due to the worsening COVID-19 situation, we favour leading hotel-chain operators with earnings upside potential in the early stages of re-opening due to (1) their strong pricing power amid reduced industry supply, (2) operating leverage and (3) better cost structure post COVID-19. Domestic hotel chains are clear beneficiaries of re-opening, and we expect occupancy rates to improve.

Chart 1: China hotel occupancy

Source: STR, Morgan Stanley Research, as of December 2022.

We favour China internet platform names exposed to niche areas such as recruitment and property solutions that could see stronger rebound after the easing of COVID controls.

The second-order derivatives relate to capital spending. In the past 18 months, capital spending in China has declined due to a lack of growth visibility during COVID-related lockdowns. We foresee corporates to expand capacity in a bid to meet the pent-up demand released by China’s reopening. We see infrastructure investment to lead the recovery cycle, and capital expenditure by private enterprises should gradually pick up upon re-opening. We also see opportunities in construction companies and related materials, as the recent property rescue package targeted the completion of stalled projects.

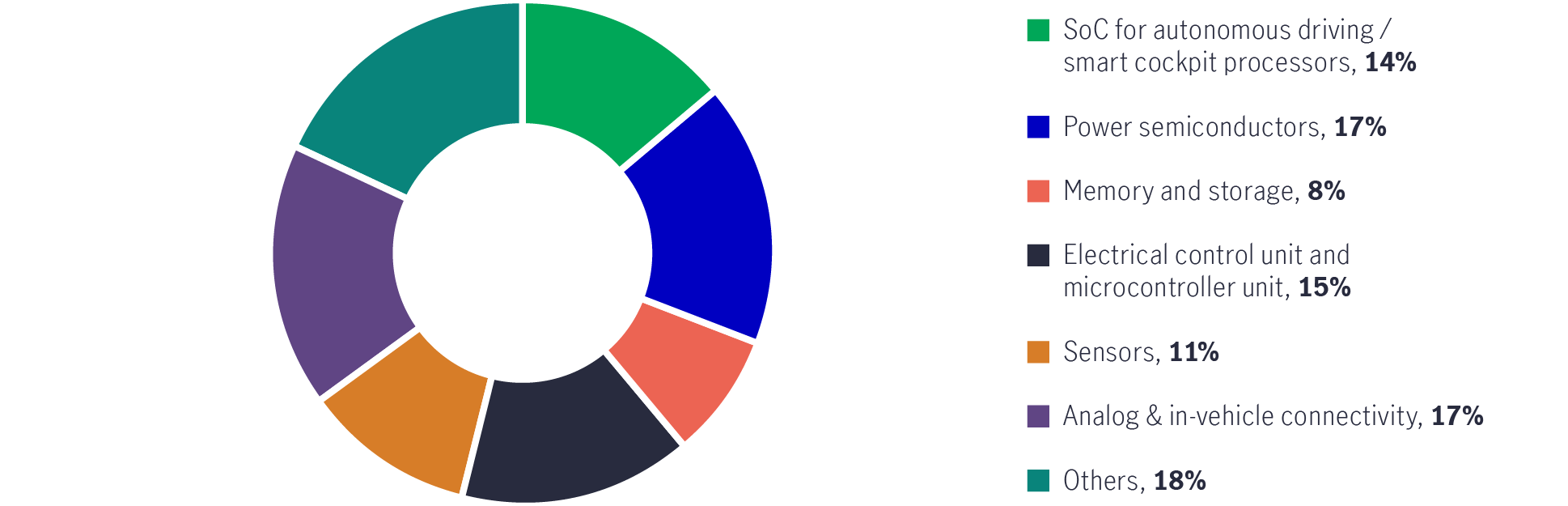

We see technology innovation and localisation opportunities in China, particularly in the semiconductor and software industries. First of all, electric vehicles (EVs) are the new drivers of the semiconductor industry, as EVs and autonomous driving are boosting demand for chips in cars. Secondly, there are various types of semiconductor products in cars with unique features that could provide significant localisation opportunities in China:

(1) System-on-chip (SoC) – IC that combines the central processing unit (CPU), graphic processing unit (GPU), memory, input/out (I/O) ports and other components on the chip.

(2) Microcontroller unit (MCU) – the most critical part of an electrical control unit (ECU) responsible for infotainment or the powertrain.

(3) Memory – higher density and bandwidth memory semiconductor chips used for autonomous driving, infotainment and network connectivity.

(4) Sensors – high resolution image sensors used in EVs.

We favour Chinese A-share semiconductor component companies, design houses and fabrication equipment suppliers that are value-chain leaders benefiting from industry growth and localisation opportunities.

Chart 2: Key areas for China’s chip makers

EVs to boost the demand for chips

Market size of auto semiconductors

Source: Manulife Investment Management, HSBC Qianhai Securities, as of July 2022. The above information may contain projections or other forward-looking statements regarding future events, targets, management discipline or other expectations. There is no assurance that such events will occur, and the future course may be significantly different from that shown here.

For the equipment market, China registered strong growth of 58% year on year (YoY) to US$29.6 billion in 2021. The localisation rate of China’s chip equipment remained low at around 10%, which presents ample opportunities for domestic companies to grow4.

In terms of software, we favour companies that are key beneficiaries of rising digitalisation across different industry verticals – in particular Software as a Service (SaaS) leaders benefitting from (1) enterprise digitalisation transformation, (2) increased demand from cost savings and (3) operating efficiencies.

According to the Ministry of Industry and Information Technology (MIIT), China’s software industry revenue grew by 9.8% YoY to RMB 6.4 trillion in the first eight months of 2022 despite a COVID-19 resurgence in China. China’s SaaS penetration in terms of total IT spending is still much lower than that of the U.S.5

By segment, IT services and security enjoy faster growth than software products and system software.

On the other hand, China’s enterprise application SaaS market is expected to grow by 22% (2021-26E CAGR) driven by an expansion of the public cloud market and rising penetration due to demand for enterprise digital transformation.

With faster software self-sufficiency amid geo-political tensions, we believe domestic software leaders may also gain market shares from foreign players.

Manufacturing upgrade is another unstoppable trend. Automation is a fast-growing industry in China, riding on the trend of labour replacement owing to: (1) rising wages and labour shortage, (2) rapid expansion of emerging end markets such as consumer electronics, automobiles, batteries, solar/semiconductors and (3) the ongoing trend of domestic substitution which drives industry growth. We favour automation-component companies that are (1) leaders in respective component segment with strong R&D capability and product pipeline, (2) vertical integration capabilities increasing ability to control costs.

The Chinese government has reiterated the importance of innovation, technological development, and manufacturing upgrades to pursue technology self-sufficiency, serving as long-term tailwinds for its advanced manufacturing industries involved in scientific and technological innovation. China will reportedly provide more than RMB 1 trillion over the next five years to subsidise its semiconductor industry6, implying a major step towards its self-sufficiency goal. Besides central government support, the industry has been increasing R&D expenditures7. In our view, increased capital expenditure will expand manufacturing capacities, and advanced manufacturing will play an essential role in localising supply chains for manufacturing import substitutes.

After a market correction in 2022, valuations of some of Taiwan’s leading tech names are beginning to look attractive. There are signs that inventory levels in Taiwan’s tech sector are beginning to bottom out (most downstream tech companies in Taiwan cut their inventory levels in the third and fourth quarters of 2022). Taiwanese semiconductor names continue to benefit from deglobalisation (some US companies are asking their supply chains to use chip parts and other components made outside of China). Several bright spots are emerging from the Taiwanese tech sector:

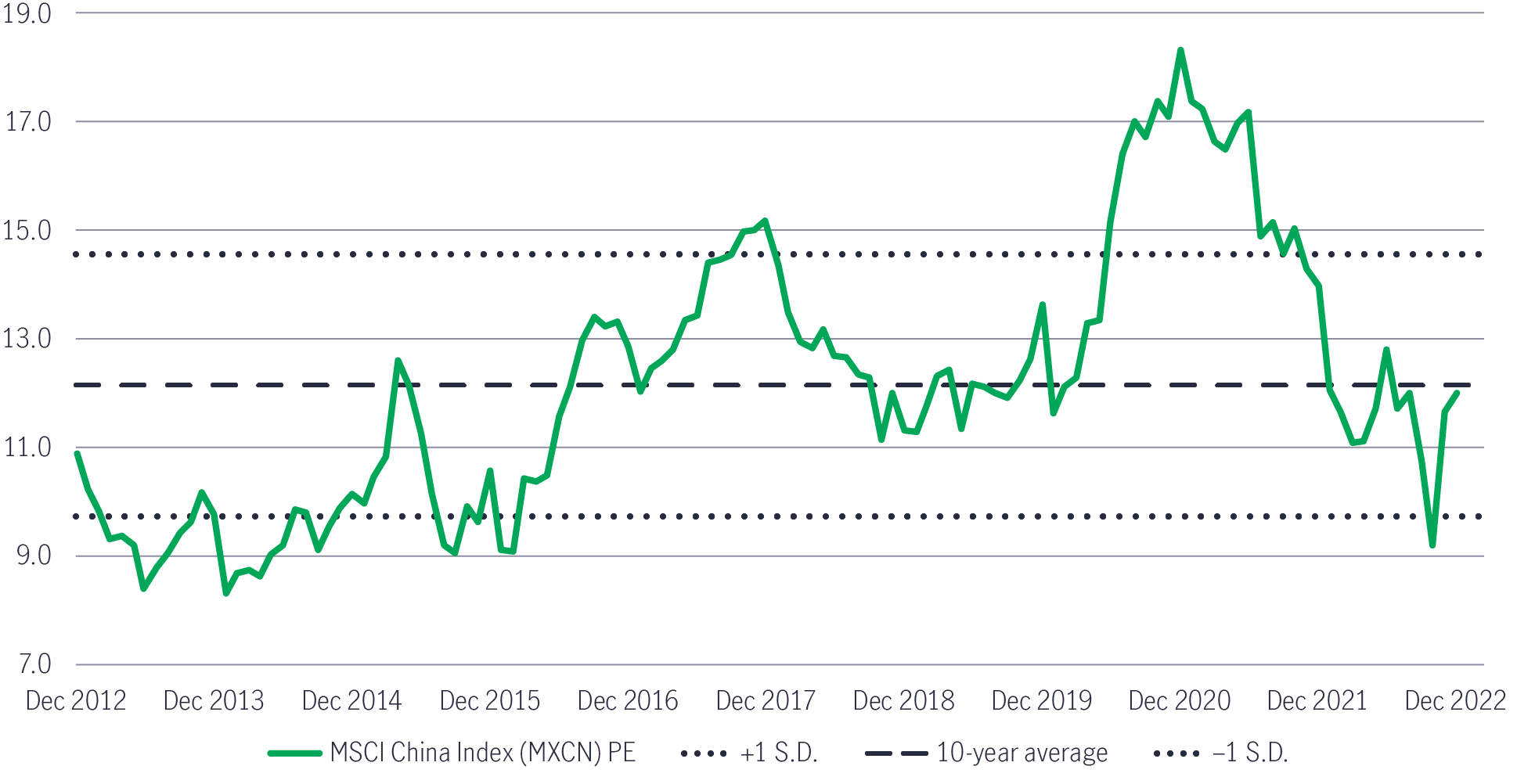

In the past year, the Greater China equity market has been affected by US interest rate rises and China’s macro and COVID-19 policies. The valuation of the broad market, MSCI China Index, now trades at 11.6 times price-to-earnings (PE), close to its 10-year historical average8. Given the Fed rate hikes are expected to slow9, and China’s economic fundamentals should gradually pick up following more reopening measures, we think Hong Kong equities (including H-shares) could see their PE multiples rise, led by the valuation re-rating cycle, with the potential of outperforming A-shares in the first quarter of this year.

Overall, we are optimistic that Greater China equities will enter a more constructive stage. While the near-term global macro-outlook remains challenging, Greater China equities are expected to see healthier fundamentals and a re-rating of valuations on the back of China’s reopening. We are encouraged by the growth opportunities derived from China’s re-opening, technology innovation/localisation, manufacturing upgrade, and Taiwan’s tech sectors.

Greater China equity markets 2022 performance2

MSCI China Index (MXCN) valuation as of 31 December 20228

1 The “three arrows” in November 2022– On 8 November, the National Association of Financial Market Institutional Investors (NAFMII) and the PBoC announced a RMB250 billion funding facility to provide support for private corporate-bond financing; On 21 November, the PBoC announced a plan to issue RMB200 billion in interest-free relending loans to commercial banks to help ensure the delivery of unfinished property projects; On 28 November, the China Securities Regulatory Commission (CSRC) announced the optimisation of five measures in equity financing to support the financing of property developers.

2 Bloomberg, Manulife Investment Management, as of 31 December 2022. It is not possible to invest directly in an index. Past performance is not indicative of future performance. All indices are rebased to 100 on 31 December 2021, except MSCI Taiwan which is rebased on 3 January 2022.

3 The Straits Times, 17 November 2022. In November, Chinese President Xi Jinping and US President Joe Biden met at the G20 Leaders’ Summit and pledged to work together to manage tensions and avoid conflict. President Xi added that both sides need to “find the right direction for the bilateral relationship going forward and elevate the relationship".

4 SEMI Equipment Market Data Subscription, July 2021.

5 Gartner, as of 2021.

6 Reuters, 13 December 2022.

7 According to a white paper published by the China Association for Public Companies (CAPCO), listed advanced manufacturers in China reported revenue growth of 20.1% YoY, with R&D expenditures increasing to RMB 642.59 billion in 2021.

8 Bloomberg. Latest PE figure is as of 10 January 2023. Based on Bloomberg’s estimated PE ratio for the next fiscal year.

9 On its 13-14 December FOMC meeting, Fed raised rates by 50bps, decelerating from its 75bps hikes in recent four months. The FOMC’s median projection expects a rate peak of 5.1% in 2023, vs. the current level of 4.25%-4.5%. US November consumer price index (CPI) also indicates easing inflation pressure, with the reading rose 7.1% YoY, lower than expected and being the lowest level since December 2021.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

© 2026 Manulife Investment Management. All rights reserved.