News confirming the lifting of lockdown restrictions is almost always greeted by a sense of relief and a healthy dose of optimism. It’s confirmation that life can finally begin to gradually return to business as usual—consumers can resume spending, jobs can return, and policymakers can turn their attention to other pressing issues. However, the great economic reopening also brings with it a series of uncertainties.

There are several reasons for this: First, economic data will be extraordinarily difficult to read; forthcoming data sets are likely to be as distorted to the upside as they've been to the downside as a result of lockdowns and social distancing measures introduced in the past year. Second, although the unprecedented disruptions and bottlenecks to global supply chains—from commodities to labor—should unwind soon (in theory), when that will actually happen remains challenging to predict with any degree of certainty. Third, as most developed economies make their way out of the COVID-19 recession, they should find themselves in the early stage of the next economic and market cycle; however, it isn’t clear whether this coming cycle will bear conventional characteristics like those we’re familiar with, particularly in view of how we got here in the first place. That said, there remains important macroeconomic pillars that can guide investment decisions, in both the near term and the long term.

Source: Manulife Investment Management’s asset allocation team, May 10, 2021. Model inputs form part of Manulife Investment Management’s research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. To initiate the investment process, the investment team formulates five-year, forward-looking risk and return expectations developed through a variety of quantitative modeling techniques and complemented with qualitative and fundamental insight; assumptions are then adjusted for economic cycles and growth trend rates. This chart may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here. The information in this material, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events for other reasons. This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any investment products or to adopt any investment strategy. It is not possible to invest directly in an index. Past performance does not guarantee future results.

With the reopening taking root in key developed economies, we find ourselves gravitating toward a cyclical expansion with reduced uncertainties. While the pace of the reopening will likely be uneven, in aggregate, we believe the global economy is on track to see broad improvements in general economic activity, from household spending to global trade. While a great deal of economic data will be distorted by year-over-year (YoY) base effects, supply chain disruptions, and the impact of stimulus measures, the risk of a global recession taking place over the next three years is much lower than it was in the three years leading into the pandemic. Further, uncertainties surrounding the virus itself are shrinking as vaccination efforts ramp up globally, albeit with some regional differences. In our view, this should allow for a gradual return to business as usual and, along with it, more traditional economic fundamentals, most of which are positive. While this doesn’t mean we can wave goodbye to periods of risk off in the market, nor does it tell us how long this next cycle will last, it does suggest that we can be generally optimistic about the economic trends in the coming years.

Broadly speaking, we expect global central banks to embark on a path toward normalization, (very) slowly unwind the extraordinary monetary policy measures introduced during the crisis—albeit at a different pace. This will likely begin with a tapering of current asset purchases in 2021/2022—a step already taken by the Bank of Canada (BoC)—which is likely to inject some volatility, as such maneuvers typically push market-based bond yields higher both mechanically and through the expectations channel. We don’t, however, expect most global central banks to hike policy rates until 2023/2024 and, combined with what’s likely to be a great deal of sovereign debt issuance, we therefore expect global yield curves to steepen. While the speed and timing of this expected yield curve steepening will matter to the broader risk market, we view this as a positive development, as it’s emblematic of a normalizing economy.

In our base-case scenario, we expect to see some near-term inflation pressure due to base effects, supply chain disruptions, and a jump in services activity as economies reopen. However, we believe these price pressures will ultimately prove to be transitory as bottlenecks ease, more labor supply comes back online, and pent-up demand fades. Our longer-term inflation model suggests inflation in most developed markets will be closer to the lower end of the 2.0% to 2.5% YoY range. That said, a protracted period of elevated commodity prices and/or labor shortage would be a key risk to our inflation outlook.

Opportunistic perspectives

Short-term asset allocation view (6–12 months)

Source: Manulife Investment Management’s asset allocation team, May 10, 2021. Model inputs form part of Manulife Investment Management’s research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. To initiate the investment process, the investment team formulates five-year, forward-looking risk and return expectations developed through a variety of quantitative modeling techniques and complemented with qualitative and fundamental insight; assumptions are then adjusted for economic cycles and growth trend rates. This chart may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here. The information in this material, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events for other reasons. This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any investment products or to adopt any investment strategy. It is not possible to invest directly in an index. Past performance does not guarantee future results.

Despite our belief that interest rates will gradually rise, they’re likely to stay near historic lows and struggle to exceed prepandemic levels, even over the course of the next few years. With muted returns expected in the fixed-income space, particularly in global government debt, asset classes that can provide additional yield are likely to find favor with investors; this is especially true for asset classes that can also provide diversification benefits. This perspective underpins some of our higher-conviction views, such as our overweight stance on emerging-market (EM) debt. It also explains why we have an improved outlook on certain alternative assets, such as real estate investment trusts (REITs).

Finally, we expect the U.S. dollar (USD) to weaken over our forecast horizon, driven by wider fiscal and current account deficits in the United States as well as a central bank—the U.S. Federal Reserve (Fed)—that’s expected to continue to provide ample liquidity and remain dovishly positioned relative to other global central banks. A weaker USD will typically translate into tailwinds for a variety of asset classes, including EM assets (both debt and equity) and select developed-market equities and fixed income.

Strategic perspectives

Long-term asset allocation view (3–5 years)

Source: Manulife Investment Management’s asset allocation team, May 10, 2021. Model inputs form part of Manulife Investment Management’s research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. To initiate the investment process, the investment team formulates five-year, forward-looking risk and return expectations developed through a variety of quantitative modeling techniques and complemented with qualitative and fundamental insight; assumptions are then adjusted for economic cycles and growth trend rates. This chart may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only as current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here. The information in this material, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events for other reasons. This material should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any investment products or to adopt any investment strategy. It is not possible to invest directly in an index. Past performance does not guarantee future results.

We continue to believe that interest rates will be moving higher as the United States and global economies reopen and central banks slowly begin the process of normalization. Crucially, we believe the Fed will keep front-end rates pinned by pushing out rate hike expectations even as it tapers asset purchases. Perhaps more importantly, investor focus should be on the long end of the U.S. yield curve; in other words, the 30-year yield, which is most at risk of climbing aggressively. Higher rates and a steeper yield curve are likely to produce material headwinds in longer duration U.S. Treasuries and act as a general drag within this asset class, particularly in the near term.

In the longer run, however, we believe market pricing will adjust appropriately to reflect expectations of moderately higher inflation and expect the rise in market rates to slow (but not stop) as we move further along this economic and market cycle. In our view, while the asset class will remain challenged (reflected by our near-term underweight stance), we believe the longer-term expected return for U.S. government bonds has improved slightly relative to October 2020.

Our overweight stance on EM debt continues to be one of our strongest-conviction views—in both the short term and the long term. From a tactical perspective, strengthening momentum behind the global economic rebound and a stall in USD strength should provide support to the asset class.

We believe EM debt will provide some of the most attractive expected total returns over the next five years within fixed income, thanks to the relatively high level of income returns the asset class offers, coupled with additional support from a weaker USD. Crucially, although we expect interest rates to rise somewhat in the coming years, they’re likely to remain near historic lows. This creates an environment that should drive more flows into EM debt as the search for yield becomes more urgent and the carry it can provide becomes more important to investors. Our conviction in what we expect to be a strong cyclical recovery also supports a solid overweight stance on EM debt, especially since regions such as Latin America are poised to benefit from global growth and rising demand for commodities, which should fare well in such an environment in the years ahead. Finally, we have a slight preference for local currency debt over USD-denominated EM debt, a view that’s consistent with our expectation for the greenback to weaken over the long term.

We expect non-North American developed-market interest rates to lag their U.S. and Canadian counterparts as major central banks such as the European Central Bank and the Bank of Japan appear even more likely to leave policy rates on hold and keep front-end rates contained. The same can be said of the broader economic recovery in light of the pace of vaccination rollout programs (with the U.K. being an exception). However, a gradual return to normalcy will inevitably push European and Japanese rates higher, particularly at the longer end, which will likely translate into headwinds in their respective bond markets. Crucially, on a currency-adjusted basis, we find Japanese fixed income slightly more attractive than European fixed income.

While we don’t expect the BoC to raise interest rates for several years, it’s important to note that it’s already begun tapering its asset purchases. Crucially, an argument can be made for the BoC to raise interest rates before the Fed, both because of Canada’s higher inflation profile and concerns about financial stability, specifically housing. That said, while the BoC may begin to raise rates before the Fed, we believe it’s likely to do so at a slower pace relative to the Fed, in light of the high levels of public and private sector debt in Canada. The end result is that—some timing questions aside—the Canadian interest-rate profile (across the yield curve) will closely resemble the United States’ interest-rate profile. If the Canadian dollar were to strengthen against the USD, as expected over the longer term, it’s fair to conclude that Canadian debt would be slightly more attractive than U.S. debt—if only marginally. By the same logic, on currency-adjusted terms, Canadian corporate credit could offer marginally higher total returns relative to U.S. corporate credit.

We have a favorable view of high-yield debt, thanks to its exposure to cyclical risk and the carry the asset class provides in the current low interest-rate environment. In our view, the income return that the asset class offers more than offsets the risks associated with price movements. Meanwhile, from a total return perspective, high-yield debt has one of the more attractive prospects in the fixed-income space. That said, spreads have already tightened significantly, and the outlook for the asset class may be slightly more muted than it was at the start of the year.

From a longer-term perspective, our view of the high-yield space is also supported by the Fed’s (and other major central banks’) recent foray into credit easing, which implies that the asset class could see some form of policy support from central banks in the event of a future crisis.

In our view, the appeal of investment-grade credit is similar to high-yield debt, which includes the ability to provide positive carry that’s likely to outweigh headwinds arising from higher interest rates and a generally favorable outlook on the back of improved growth. Importantly, from a total return perspective, we think high-yield credits are more attractive than investment grade, but it’s also worth noting that investment-grade debts can be used as a tool for investors to add duration to their portfolios. Within this space, we have a preference for lower-rated credits but also believe it’s important to keep an eye on cross-country opportunities.

Since October, short-term risks that had once threatened to hurt sentiment—from the presidential election’s outcome to fiscal stimulus to the vaccine rollout—have been resolved. These developments, along with ample liquidity and expectations of strong growth, have contributed to the asset class’s strong performance. We remain optimistic about the country’s growth outlook for the next several quarters and therefore remain constructive on U.S. equities. However, our view is tempered by high valuations and the likelihood that excitement regarding the reopening trade could soon migrate to other regions as they catch up to the United States. Moreover, given already robust investor expectations relating to the asset class and the macro backdrop, the bar to positive surprises could be fairly high. Over the next several months, we could well see a more granular, sector-level view emerge that we believe will be critical for any outperformance.

On a structural basis, the United States has the healthiest long-term economic profile in the developed world; however, stock valuations and an expected dollar depreciation (particularly against other key developed-market currencies) remain modest headwinds for the asset class.

While the asset class is increasingly weighted toward technology, it remains levered to manufacturing and the global trade impulse, which we expect to remain strong over the next few quarters. Recent concerns about the cooling Chinese macro backdrop have affected Chinese equities and caused the broad asset class to lag, but improved market sentiment following an overly negative market reaction could lead to a period of outperformance in China. Meanwhile, markets such as South Korea and Taiwan provide exposure to semiconductors, which should continue to benefit from the global recovery.

In our view, EM equities remain attractive from a long-term valuation perspective. We expect this asset class to retain a robust growth profile and continue to provide an attractive dividend profile throughout the duration of our five-year forecast period. Understandably, a structurally weaker USD could provide a modest tailwind to this asset class

Our tactical view of European equities (including U.K. stocks) has become increasingly favorable as the region moves closer to more normalized activity even as valuations remain low relative to the United States. Meanwhile, continued fiscal and monetary policy support has provided a buffer against the worst of the lockdown-related restrictions, while the region’s manufacturing sector continued to perform well.

We continue to find the asset class attractive from a strategic perspective in terms of valuation and its dividend profile. A strengthening euro and a cyclical upturn over the next four to six quarters could translate into additional modest tailwinds; however, this favorable profile is partly offset by the region’s weak growth profile over the longer term.

Continued progress on the vaccination front is encouraging, while higher oil prices and a steeper yield curve should continue to support the energy and financials sectors, which make up a significant part of the S&P/TSX Composite Index. While it’s likely that investors could revisit concerns relating to the real estate market and consumer indebtedness in the medium term, we expect the next few quarters to be dominated by excitement relating to the great reopening. That said, any sign that the BoC might be adopting a more hawkish stance could inject some volatility into the market, particularly on the foreign exchange front.

Despite a weaker long-term growth profile, we continue to find Canadian equities attractive for the following reasons: a supportive dividend profile, reasonable valuations, and a somewhat modest tailwind from the Canadian dollar’s expected appreciation.

In theory, Japanese equities should appeal to investors; after all, the asset class should benefit from pro-cyclical growth, a weaker yen, and continued massive monetary and fiscal support. In practice, muted foreign demand meant that returns from the asset class remained somewhat disappointing in recent months—if that changes, we could well experience a period of outperformance.

In our view, structural factors in favor of Japanese equities include inexpensive valuation, continued improvement in corporate governance, and generous share buyback programs, but these factors remain more of an offset to what’s a muted growth profile. From a three- to five-year perspective, we continue to have a neutral view of the asset class, albeit with a mild positive bias.

A recent weakening in key macroeconomic data has led to speculation that China’s growth profile has peaked, causing the MSCI China Index to lag other equity markets over the last few months. We expect this moderation to continue, particularly as the economic recovery transitions from being manufacturing led to more services led. However, a recent shift in sentiment would suggest short-term support for this asset class as it recovers from overly negative sentiment.

We’ve long maintained that Chinese growth will need to decelerate gradually in order to facilitate a rebalancing from its industrial growth model to a consumer growth model. While the COVID-19 outbreak has been disruptive, we believe the official policy response will be meaningful enough to keep China in that pattern over the next five years. As a result, we no longer expect the country to benefit from valuation expansion relative to the rest of the world, including EM. We also expect the renminbi to depreciate modestly over the next three to five years.

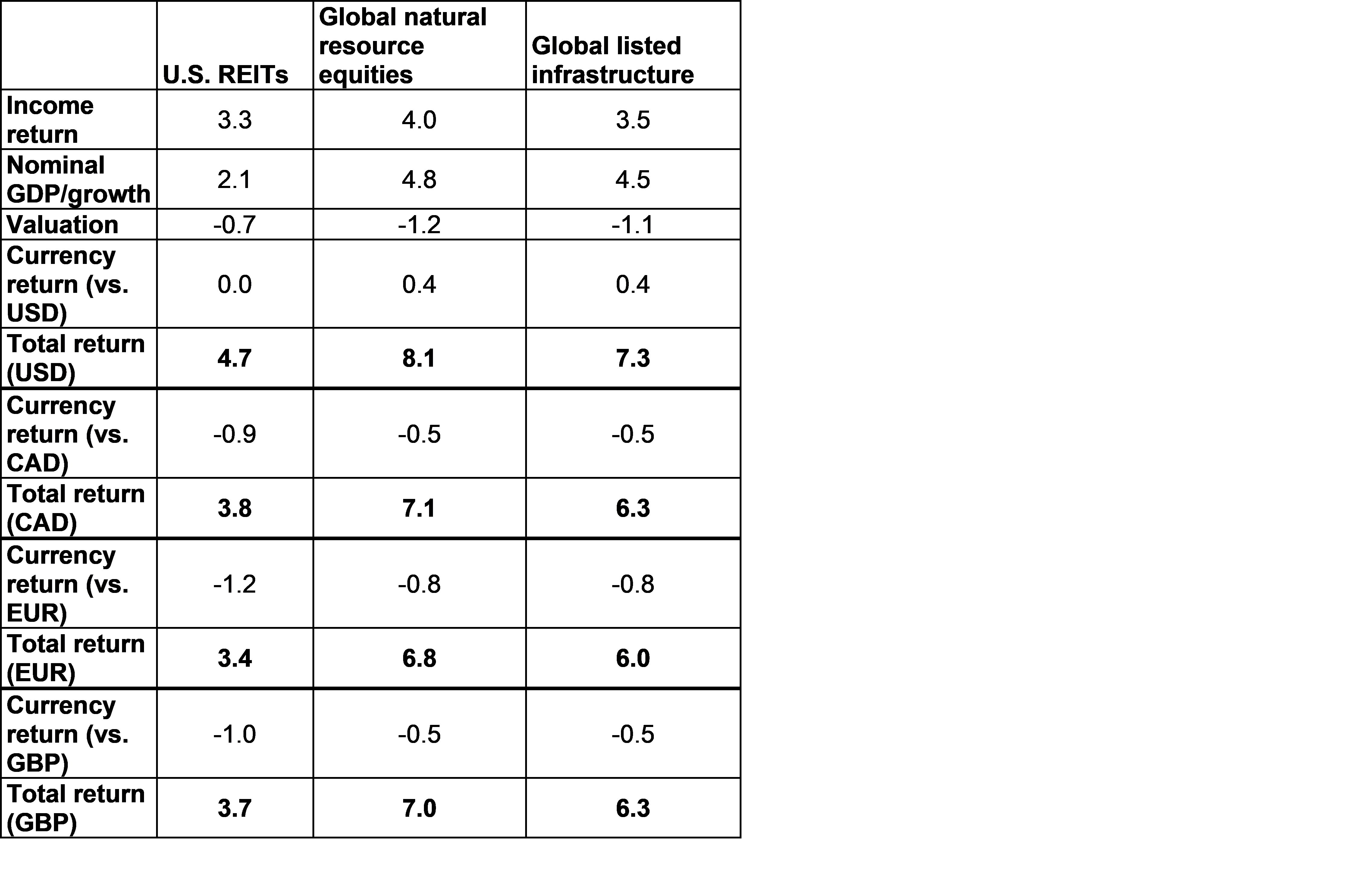

We’ve upgraded our views on U.S. REITs, as the great reopening and the improving macro backdrop are likely to be constructive for the asset class. Broadly speaking, we believe that the asset class’s key characteristics continue to appeal in the current environment—it has an income component in addition to offering dividend yields that are more attractive relative to both real assets and financial assets. Crucially, REITs also enjoy low correlations to other asset classes, particularly fixed-income assets, and therefore offer potential diversification benefits.

However, the subsectors within the REIT universe are highly bifurcated—we expect those in the industrial, residential, and data center segments to continue to fare well but recognize the uncertainty confronting those in the retail and office space. In addition, we foresee uncertainty developing in the longer term as household and business preferences evolve over time and believe that could affect the demand of certain subsectors within the real estate complex. For this reason, we continue to have a neutral stance on the asset class despite the presence of several favorable dynamics. That said, while rising interest rates could curb the appeal of the asset class, they don’t—in our view—represent a headwind that would wipe out any potential benefits that REIT investors could gain from the great reopening.

The faster-than-expected reopening in the United States saw a corresponding rise in car journeys, providing support for crude oil in the short term. We expect to see a similar picture in Europe and other developed markets as they gradually reopen, although it could be some time before EM economies (e.g., India, Latin America) could resume business as usual, thereby preventing demand from spiraling in the near term. Global appetite for lumber, however, continues to outstrip supply due to bottlenecks at sawmills, causing prices to rise significantly in recent weeks.

Equity valuation within the global natural resource space has mainly been driven by the energy component, which could continue. In our view, global natural resource equities are an example of a cyclical play and should outperform global equities at this point in the economic cycle.

Source: Manulife Investment Management’s asset allocation team, as of May 6, 2021. Model inputs form part of Manulife Investment Management's research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. Projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here. TIPS refers to Treasury Inflation-Protected Securities.

Source: Manulife Investment Management’s asset allocation team, as of May 6, 2021. Model inputs form part of Manulife Investment Management 's research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. Projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different than that shown here. EAFE refers to Europe, Australasia, and the Far East.

Source: Manulife Investment Management’s asset allocation team, as of May 6, 2021. Model inputs form part of Manulife Investment Management's research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. Projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here.

Source: Manulife Investment Management’s asset allocation team, as of May 6, 2021. Model inputs form part of Manulife Investment Management's research and are not meant as predictions for any particular asset class, mutual fund, or investment vehicle. Projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations are only current as of the date indicated. There is no assurance that such events will occur, and if they were to occur, the result may be significantly different from that shown here.

Important disclosure

A widespread health crisis such as a global pandemic could cause substantial market volatility, exchange-trading suspensions and closures, and affect portfolio performance. For example, the novel coronavirus disease (COVID-19) has resulted in significant disruptions to global business activity. The impact of a health crisis and other epidemics and pandemics that may arise in the future could affect the global economy in ways that cannot necessarily be foreseen at the present time. A health crisis may exacerbate other preexisting political, social and economic risks. Any such impact could adversely affect the portfolio’s performance, resulting in losses to your investment.

Investing involves risks, including the potential loss of principal. Financial markets are volatile and can fluctuate significantly in response to company, industry, political, regulatory, market, or economic developments. These risks are magnified for investments made in emerging markets. Currency risk is the risk that fluctuations in exchange rates may adversely affect the value of a portfolio’s investments.

The information provided does not take into account the suitability, investment objectives, financial situation, or particular needs of any specific person. You should consider the suitability of any type of investment for your circumstances and, if necessary, seek professional advice.

This material is intended for the exclusive use of recipients in jurisdictions who are allowed to receive the material under their applicable law. The opinions expressed are those of the author(s) and are subject to change without notice. Our investment teams may hold different views and make different investment decisions. These opinions may not necessarily reflect the views of Manulife Investment Management or its affiliates. The information and/or analysis contained in this material has been compiled or arrived at from sources believed to be reliable, but Manulife Investment Management does not make any representation as to their accuracy, correctness, usefulness, or completeness and does not accept liability for any loss arising from the use of the information and/or analysis contained. The information in this material may contain projections or other forward-looking statements regarding future events, targets, management discipline, or other expectations, and is only current as of the date indicated. The information in this document, including statements concerning financial market trends, are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Manulife Investment Management disclaims any responsibility to update such information.

Neither Manulife Investment Management or its affiliates, nor any of their directors, officers, or employees shall assume any liability or responsibility for any direct or indirect loss or damage or any other consequence of any person acting or not acting in reliance on the information contained here. All overviews and commentary are intended to be general in nature and for current interest. While helpful, these overviews are no substitute for professional tax, investment, or legal advice. Clients should seek professional advice for their particular situation. Neither Manulife, Manulife Investment Management, nor any of their affiliates or representatives is providing tax, investment, or legal advice. This material was prepared solely for informational purposes, and does not constitute a recommendation, professional advice, an offer, or an invitation by or on behalf of Manulife Investment Management to any person to buy or sell any security or adopt any investment strategy, and is no indication of trading intent in any fund or account managed by Manulife Investment Management. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Diversification or asset allocation does not guarantee a profit or or eliminate the risk of loss in any market. Unless otherwise specified, all data is sourced from Manulife Investment Management. Past performance does not guarantee future results.

Manulife Investment Management

Manulife Investment Management is the global wealth and asset management segment of Manulife Financial Corporation. We draw on more than a century of financial stewardship to partner with clients across our institutional, retail, and retirement businesses globally. Our specialist approach to money management includes the highly differentiated strategies of our fixed-income, specialized equity, multi-asset solutions, and private markets teams—along with access to specialized, unaffiliated asset managers from around the world through our multimanager model.

This material has not been reviewed by, and is not registered with, any securities or other regulatory authority, and may, where appropriate, be distributed by the following Manulife entities in their respective jurisdictions. Additional information about Manulife Investment Management may be found at manulifeim.com/institutional.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

© 2026 Manulife Investment Management. All rights reserved.