12 January, 2021

In this 2021 outlook, Asian Fixed Income team led by Endre Pedersen (Chief Investment Officer, Asia ex-Japan) and Murray Collis (Deputy Chief Investment Officer, Asia ex-Japan) talks about why they envisage that Asian fixed income can continue to perform on the back of a supportive global backdrop and continued policy support.

Amidst a challenging 2020, Asian fixed income turned in a resilient performance1, 2. With the global spread of COVID-19 accelerating in the first quarter of 2020 leading to lockdowns globally, the virus roiled economies and financial markets. Asia was not spared: the region’s GDP was expected to take a hit that surpassed even that of the 1997 Asian Financial Crisis; however, North Asian economies contained the virus better with many expected to post positive growth in 2020 (such as China, Taiwan, South Korea). With significant monetary and fiscal stimulus, however, the region’s economies and financial markets gradually recovered over the year.

Entering 2021 we envisage that Asian fixed income can continue to perform on the back of a supportive global backdrop and continued policy support. With better fundamentals than its peers, we feel the asset class is poised to be in a better shape for potential upside, anchored to Asia’s resilient credit profile and burgeoning multi-year sustainable investing opportunities in Asia.

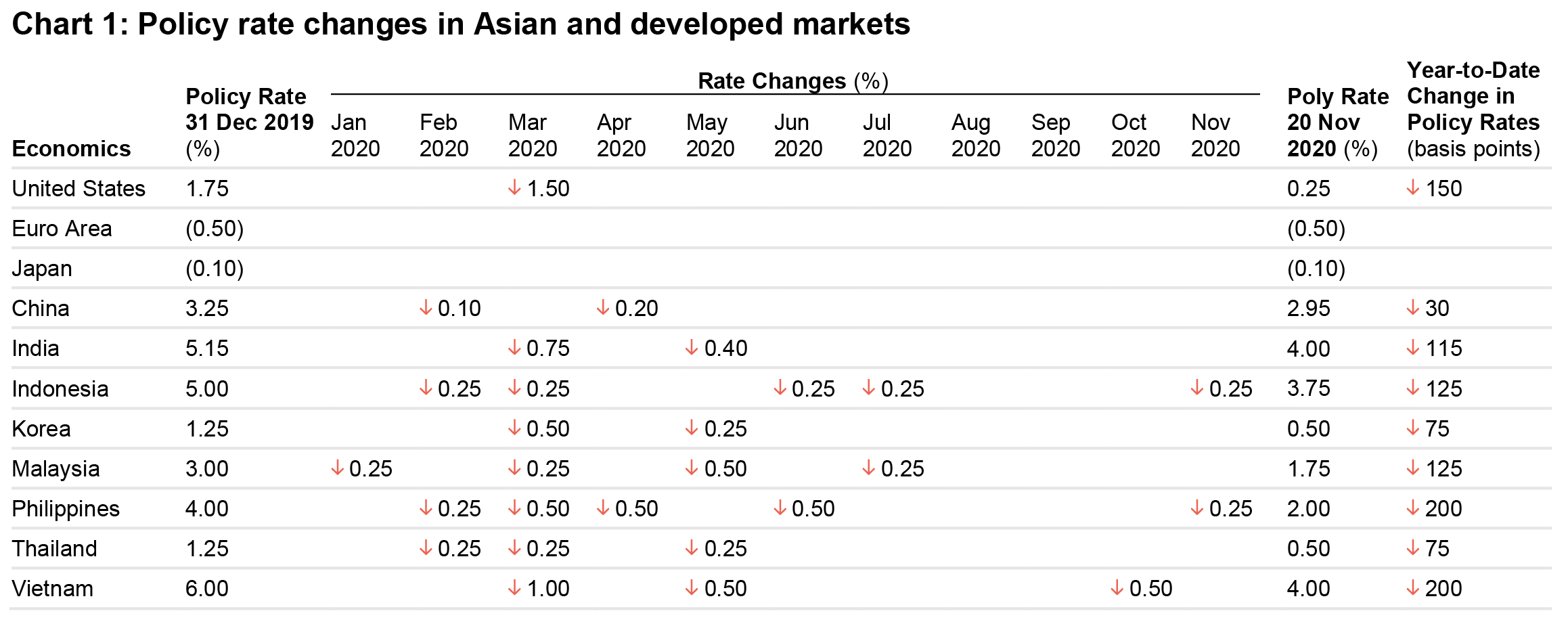

Despite the notable challenges of the past year, the fundamentals of Asian fixed income remain intact. The asset class remained resilient throughout the year delivering positive performance. During the first quarter of 2020, the JP Morgan Asia Credit Index (JACI) corrected around by 8-9% (to the trough), as the pandemic dented global financial markets. It also exhibited a lower drawdown relative to US credit markets 1 . As more global monetary and fiscal stimulus came into place, the Asian credit market then experienced a sharp-but-steady rebound of about 12% (from low to high) towards the end of 2020. Indeed, the aggressive rate cuts and market stimulus provided by the US Federal Reserve provided cushion for Asian central banks to follow suit (see Chart 12 ). Most Asian currencies also stabilised and strengthened on the back of a weaker US dollar as global rush-to-safety capital flows receded3 .

As the pandemic’s impact on credit markets also varied across different markets and industries, we saw an increasing divergence in credit quality. That said, the region is in a relatively better position due to the unique structure of JACI, where a majority of issuers are investment grade with many state-owned enterprises and quasi-sovereign entities benefitting from a diversified range of funding channels including the local banks and bond markets.

In the high-yield space, while defaults have indeed ticked higher, the impact has been less pronounced than initially feared4. For instance: full-year default forecasts for Asian high-yield have been revised lower from 4% in July to 3% in October 5 . Furthermore, the region has thus far only seen about 1.4% of investment-grade credits turn into “fallen angels”– only marginally higher than the 10-year average at 1.2%4 .

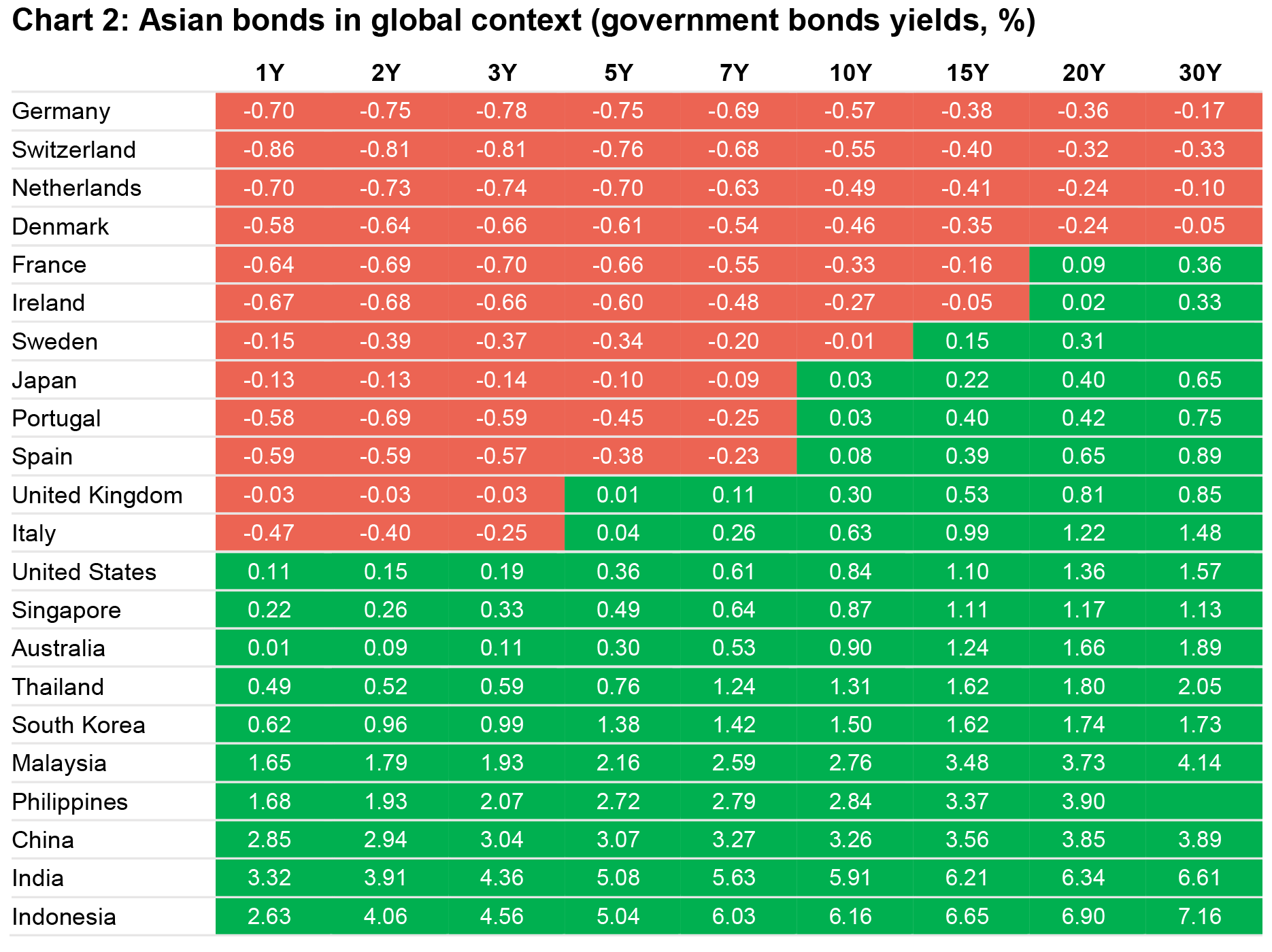

The more favourable macro landscape in 2021 should be constructive for Asian fixed income. We are positive on the broader Asian fixed income landscape given its resilient credit fundamentals, continued accommodative monetary and fiscal policy, and downward pressure on the US dollar. As mentioned, aggressive rate cut and unprecedented balance sheet expansion by global central banks, more and more developed market government bonds become negatively-yielding (Chart 26 ). In the event of “tail-risk-event”, i.e. US Treasury yields to turn negative in 2021 (e.g. a delay with the distribution of vaccine, or deflationary environment), we could see a major asset-rotation among bond and income investors, driven by the ongoing search for “positive” yields, making Asian bonds stand out given their sound fundamentals.

Overall, we expect defaults to remain reasonably contained and idiosyncratic in the first half of 2021 before an improvement in the second half as vaccines roll out globally, and Asia’s US dollar bond market is ready for re-financing issues, which are conducive to improve risk sentiment. Having said that, credit selection will remain key in Asian markets, as the recovery is expected to uneven across countries and sectors.

China’s impressive economic recovery should continue: real GDP growth for China is forecast to accelerate from 2% in 2020 to 8.2% (year-on-year) in 2021, before falling back to trend growth (5-6%) range in the following year7 . Riding on optimism that the rollout of vaccines will help to support a return to global growth and broader economic recovery in China, we could see China withdraw some of the highly expansionary credit and fiscal policies implemented during 2020 to counter the pandemic. Policy rates are expected to remain relatively stable as the People’s Bank of China (PBOC) has consistently signalled that it is against excessive stimulus. It will likely continue with targeted monetary policy actions that could include more targeted reserve ratio requirement (RRR) cuts, as well as open market operations, to manage market liquidity.

China bonds stand out in the current market cycle, relative to other global bond markets, due to its high nominal and positive real yields and diversification opportunities. In the current macroenvironment and credit down cycle, we believe capturing the most attractive income opportunities with credit selection is key.

As 10-year CGB yields have now moved back to around the 3.3% level, we believe this is an attractive entry point for investors and now offers a very decent pick-up of around 2.4% against US treasuries8 . From a curve perspective, the 5–7-year segment looks particularly attractive compared to longer-dated paper in terms of relative value. We believe the renminbi will stay broadly around current levels with the potential to appreciate further against the US dollar targeting the 6.40 level in the first half of 2021, after appreciating against the US dollar by 6% in 2020. This is driven primarily by the softness in the US dollar that may weaken further on possible delays to the US economic recovery. We remain focused on systemically important state-owned enterprises that are also less reliant on the US from both an operational and funding perspective. Domestically concentrated sectors, such as utilities, property, telecommunications and media, are also areas of focus.

The tail risks stemming from continuing USChina tensions will likely persist – especially given recently passed legislation authorising the potential delisting of US-listed Chinese firms. Also, we see increased tolerance on the part of Chinese regulators to orderly allow some bondholders to take losses, particularly for less strategically important stateowned enterprises.

Turning to Indonesia, the country arguably suffered the most economically among regional markets, posting its first negative year-on-year growth and technical recession since the Asian Financial Crisis. In response, the Indonesian government and Bank Indonesia released unprecedented levels of stimulus, including the use of debt monetisation. These unique policy tools helped to boost economic growth and maintain confidence in the country’s credit markets. At the sovereign level, its current credit ratings (BBB, stable outlook by Moody’s and Fitch) provide it with an ample buffer against being pushed below investment grade. Major quasisovereign corporates and leading banks also feature resilient credit metrics with adequate liquidity, making them well-positioned to retain their investment-grade ratings. Although the Indonesian rupiah experienced a volatile 2020, it is potentially poised for more stable performance in 2021 on the back of the country’s stronger economic prospects – this is despite the nation’s reliance on external debt. Within the high-yield space, quality high-yield issuers with adequate liquidity and decent corporate governance appear well positioned.

For India, fallen-angel risks are on our radar as bank non-performing loans (NPLs) are expected to rise to double-digits over the next 12 to 18 months 9 . However, the risks are mitigated by the improvement in COVID-19 containment (e.g., a 69% decline in active cases since mid-September10 compared to an increase in the rest of the world in general) and its resilient financial-sector metrics. This would be supportive of macro-economic recovery in 2021. From a fiscal policy perspective, India has increased debt to support the economy; however, despite having a debt-to-GDP ratio approaching 90%, we are less worried as external debt only comprises about 20% of GDP11, which is considered to be at the lower end of the spectrum among emerging-market economies. In India, “national champion” stateowned enterprises are likely well positioned, as well as renewables with strong parent supports.

This theme of careful credit selection also extends to a major emerging opportunity – ESG investing.

Although Asia arguably emphasised ESG later than other regions such as Europe, recent trends show momentum and optimism for investors in the space. With China, Japan, South Korea, Hong Kong, and New Zealand committing to becoming carbon neutral12, and other governments are likely to follow, we expect to witness a greater number of greenbond issuance. Global green bond issuance grew 12% in 2020 compared to the first nine months of 2019 and the global trend is supportive of further growth in the green and sustainable-labelled bond segment13.

Beyond this trend, another reason investor should favour opportunities in this space is the ability to generate genuinely holistic returns beyond just traditional financial metrics. Outperforming a benchmark now is more multi-faceted than simply looking at the differences in returns, but also includes ESG factors, such as carbon intensity (E), ability to provide aging population support (S) or stronger governance structures (G). If a certain sustainable portfolio matches the benchmark but does so with significantly less carbon emissions, this could support climate objectives. Even from a strict financial return perspective, research and evidence suggest sustainable investing does not compromise returns (see Chart 314). For instance, the cumulative risk-adjusted return for the J.P. Morgan ESG Asia Credit Index from December 2012 to November 2020 is on par with the JACI (upper chart), from a carbon intensity perspective, JACI’s constituents emit nearly 420 tonnes of carbon dioxide (CO2) for every US$1 million of sales generated. In contrast, constituents of the J.P. Morgan ESG Asia Credit Index emit only 196 tonnes of CO2 per US$1 million of sales.

This reinforces our belief that sustainable investing can enhance returns going forward, and the performance on ESG issues will likely resonate with investors who are concerned about sustainability. More importantly, impending changes to regulation, coupled with growing investor demand for sustainable solutions, are likely to change relative performance drivers going forward. We also expect green and sustainable -labelled bonds to be held by established, longer -term institutional investors. This could establish a more stable investor base, which could help to reduce drawdown and provide better risk -adjusted returns for the asset class.

In terms of specific ESG opportunities in Asia, investors should look for companies that will benefit from environmental or social trends such as providing cleantech that will help to mitigate climate change or demographic shifts. Besides environmental and social factors, investors shall emphasise the importance of governance factors. From a governance perspective, investors should focus on companies with more independent and diverse boards while rejecting those with a history of mismanagement or opaque business models.

All in all, we believe Asian fixed income portfolios should not only consider ESG risks but actively take advantage of the ample ESG opportunities. While 2020 was an important year for ESG in Asia, we expect even more in 2021, as investors and companies explore innovation in this space.

1 Bloomberg, as of 23 March 2020. The JP Morgan Asia Credit Index (JACI) corrected by 8.79%, while the ICE BofA US Corporate Index corrected 15.14% over the same time period. As of 23 December 2020, the JACI had gained 12.32% from its low point.

2 Central bank websites, as of 20 November 2020. 1-year medium term lending facility rate is used for China (market players use the 1-year medium term lending facility rate as a guide for the monetary direction of People’s Bank of China,

3 JP Morgan Asia Dollar Index gained 3.7%, as of 17 December 2020.

4 Although defaults in the high-yield space have hit a record US$8.8 billion, robust issuance means the default rate has been kept in check at a mere 2.4%. The percentage of high-yield paper trading at distressed levels (below 70 cents on the dollar) has moderated from 14% in March to 2% in October 2020. JP Morgan, October 2020.

5 JP Morgan, as of October 2020.

6 Bloomberg, Manulife Investment Management, as of 30 November 2020.

7 Bloomberg consensus as of December 2020.

8 Bloomberg consensus as of December 2020.

9 For Indian banks, projected NPL ratios and credit costs have been revised downward, and collection rates have spiked to 90% in October from just 50–60% a few months prior.

10 The Center for Systems Science and Engineering (CSSE) at Johns Hopkins University.

11 CEIC, yearly figure as of March 2020.

12 "Asian giant's carbon pledges boost global climate action, says UN climate chief", Straits Times, 4 November 2020.

13 Another bumper year sees green bonds push through the $1tn mark, PV Magazine, 6 October 2020.

14 Bloomberg, 30 November 2020. Figures shown are in gross USD terms. Past performance is not indicative of future results. Investment involves risk. The J.P. Morgan ESG Asia Credit Index (JESG JACI) tracks the total return performance of the Asia ex-Japan USD-denominated debt instruments across the Asian Fixed Income asset class, including floating, perpetual, and subordinated bonds issued by Sovereign, Quasi-Sovereign and Corporate entities. The index applies an Environmental, Social and Governance (ESG) scoring and screening methodology to tilt toward green bond issues or issuers ranked higher on ESG criteria, and to underweight or remove issuers that rank lower. *Carbon intensity data sourced via Trucost ESG Analysis. Carbon intensity refers to Scope 1 & 2 Tons CO2 equivalent emissions per million USD revenues.

2026 Global healthcare equities outlook: Innovation supports healthcare’s long term case

Global healthcare equities showed resilience amid 2025 volatility. The defensive characteristics, coupled with remarkable therapeutic innovations in the biopharmaceutical, MedTech, and tools sub-segments of this sector, will continue to be rewarded with capital appreciation over a full market cycle. Current valuations relative to the broader market make for an attractive entry point today, and periods like this tend to lead to outperformance for healthcare stocks over the long term.

Semiconductors poised for long-term growth amid AI boom

The global semiconductor industry remains strong – arguably the most robust we have seen in over three decades. This strength is supported by cutting-edge innovation, rising revenues and robust capital spending. While risks remain, the outlook for 2026 appears constructive, with demand for artificial intelligence (AI) applications showing few signs of slowing. Beyond AI, the non-AI markets could be poised for positive revisions as cyclical recovery gains traction after several years of consolidation.

2026 Outlook: Clearer picture, better growth

This year’s outlook spotlights a world in flux – U.S. stimulus, Europe’s rebound, China’s policy pivots, and Japan’s innovation surge all shape a landscape full of both opportunities and challenges.

© 2026 Manulife Investment Management. All rights reserved.