19 April, 2023

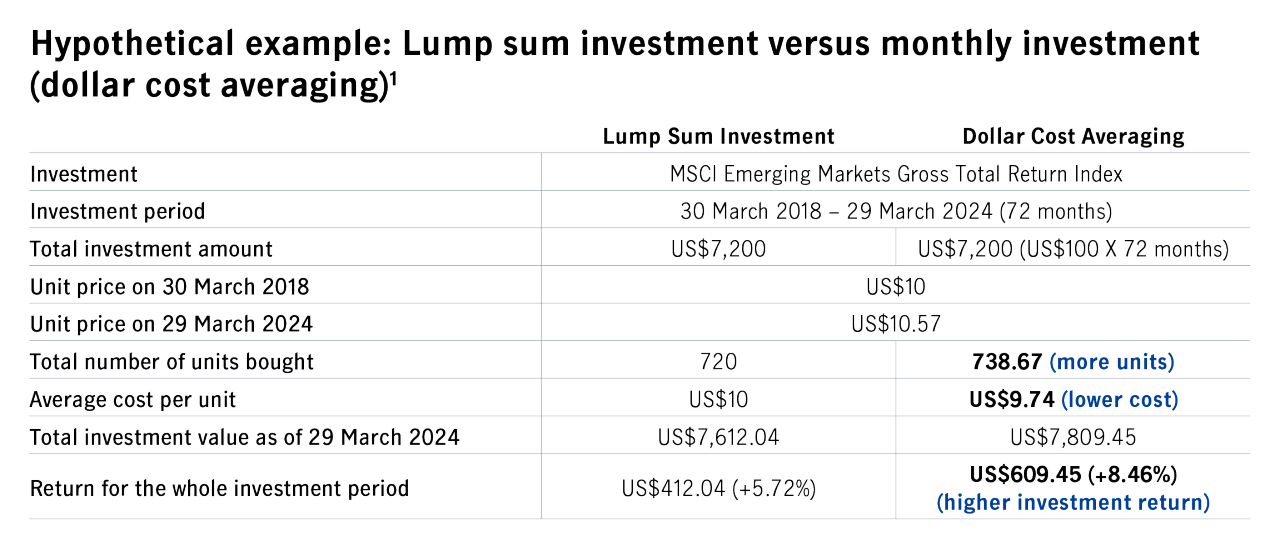

Can you predict the increase (or decrease) in the closing value of the emerging-market equity index three years from now? Without a crystal ball, it is impossible to correctly estimate future market trends, not to mention the ability to identify the best time to invest. If investors wish to reduce volatility and benefit from long-term growth when the markets move up and down, the automatically executed strategy of dollar cost averaging may be a feasible choice.

It is the practice of regularly investing a fixed dollar amount in a specific investment – regardless of fluctuations in the market price. As a result, an individual buys more units when prices are low and fewer units when prices are high.

Financial markets fluctuate, so it is often difficult to choose the best time to invest.

No single investment strategy guarantees easy profits or significant returns. So, it’s important to find a viable long-term approach that matches your risk appetite, financial goals, and budget. Here are the merits of dollar cost averaging:

However, if financial markets move higher for a prolonged period, this strategy may sacrifice the potential gains from an initial lump-sum investment.

Disadvantages of fixed deposit: is fixed income a better option?

What is a Fixed Deposit? What is Fixed Income? We explain why is fixed income now a potentially better option than fixed deposits.

Seven questions about dividends

Dividends can be a significant source of returns for equity investors. What are dividends? How do dividends fit into portfolio construction?

How to boost your income with these options

With rising inflation, earning cash deposit rates may not be enough. We look for sources of income. Discover options to boost your income before it's too late!

For illustrative purposes only.

Source: Bloomberg and MSCI, as of 31 January 2023. Total returns in US dollars. Index value is rebased as US$10 (initial unit price) on 28 February 2018. Monthly investment is made on every month end at rebased unit price. As of 28 February 2023, the geographical allocations of MSCI Emerging markets index are as follows: China (32.11%), Taiwan (15.26%), India (13.23%), South Korea (11.74%), Brazil (5.05%) and others (22.61%). The example mentioned is for illustrative purpose only. The information neither indicates any actual portfolio holdings nor constitutes any investment recommendation or advice. Different investments have different volatile patterns. Past performance is not an indicative of future performance.

Source: Bloomberg and MSCI, as of 31 January 2023. Total returns in US dollars. Index value is rebased as US$10 (initial unit price) on 28 February 2018. Monthly investment is made on every month end at rebased unit price. As of 28 February 2023, the geographical allocations of MSCI Emerging markets index are as follows: China (32.11%), Taiwan (15.26%), India (13.23%), South Korea (11.74%), Brazil (5.05%) and others (22.61%). The example mentioned is for illustrative purpose only. The information neither indicates any actual portfolio holdings nor constitutes any investment recommendation or advice. Different investments have different volatile patterns. Past performance is not an indicative of future performance.

The lump-sum approach could be more familiar to investors, many of whom already have relevant experience with equities, bonds, and funds. While both strategies have their own unique characteristics, returns may vary significantly under different market conditions. Market consensus leans towards a belief that if asset prices keep rising, then lump-sum investing can provide better returns for calm and seasoned investors, but we should also bear in mind that:

Time in the market will almost always be better than timing the market. Investment is a long-term venture that can potentially reward the patient with positive returns, while impulsive investors may experience losses.

Dollar cost averaging provides investors with a disciplined investment strategy that is easy to apply. Once the instruction is set, this approach automatically allocates regular fixed amounts regardless of market conditions and psychological factors, which helps avoid erroneous decisions. If investors believe this strategy could help them achieve their goals, they should actively identify assets with long-term growth potential and initiate a monthly investment plan.

Better Income

A “Better Income” approach seeks to understand an investor’s investment objective alongside the underlying risk of certain levels of income generation. “Better” income may not refer to the highest income level but the stability and consistency of reasonably higher yields generated throughout various market cycles.

Dollar cost averaging and its benefits

If investors wish to reduce volatility and benefit from long-term growth when the markets move up and down, the passive strategy of dollar cost averaging may be a feasible choice.

Strike a balance in life, and most importantly, in your portfolio!

A balanced asset allocation usually provides investors with a smoother investment experience and perhaps helps protect them from selling equities after they have already fallen in price. If you believe that we are likely to enter a period of further economic weakness, we’re likely to be reminded of the importance of bonds in a portfolio.

©1999 - 2024 Manulife Investment Management (Hong Kong) Limited